China opened the week with a familiar but increasingly important contradiction.

On one hand, there are tentative signs that the country’s long-running property crisis may finally be easing at the margins. On the other hand, a fresh batch of official April data showed broad economic weakness across investment, retail sales, and industrial output. At the same time, Washington and Beijing appear to be patching over parts of their trade relationship through new agricultural purchase commitments, even as pressure builds for another round of trade action focused on Chinese overcapacity.

And then there is the technology story, which increasingly sits apart from the broader economy. Even as much of China wrestles with stagnation, another China continues to advance rapidly in strategic sectors such as semiconductors, electric vehicles, drones, and artificial intelligence.

That split matters. It helps explain how China can look deeply fragile and formidably competitive at the same time.

Table of Contents

- The property market shows signs of stabilization, but the system remains badly damaged

- April economic data was worse than expected

- US-China trade finds some common ground in agriculture, but frictions remain

- The two Chinas: stagnation in one economy, rapid technological advance in another

- Anthropic’s warning: the West could lose its AI lead within two years

- China’s AI video firms are moving fast, and in some areas they may already be ahead

- The bigger picture

- FAQ

The property market shows signs of stabilization, but the system remains badly damaged

China’s property crisis may be entering a new phase. Not recovery in any meaningful sense, but perhaps the beginning of a floor.

Fresh official data from the National Bureau of Statistics showed that home price declines eased for a third straight month in April. New home prices across 70 major cities fell 0.19 per cent from March, the smallest monthly decline in a year. Existing home prices, which are often treated as a better indicator of real market conditions because they face less policy distortion, fell 0.23 per cent. That was also the mildest decline in some time.

That has prompted cautious optimism from some analysts, including at major global banks, who now think the sector may be approaching a bottom after nearly five years of crisis.

Caution is the operative word here.

The rate of decline has slowed, but prices are still falling. These are also official numbers, which means they should be handled carefully. Even if the data is directionally useful, it does not justify the conclusion that the property sector is healthy again. It is not.

The scale of the damage is still extraordinary.

- At its peak, real estate and related sectors accounted for roughly 25 to 30 per cent of China’s GDP.

- That share is now likely closer to 10 to 14 per cent.

- For many years, property represented an estimated 70 to 90 percent of household wealth.

- Since the downturn began in 2021, roughly $20 trillion in household wealth has effectively been erased.

- New home sales by value have fallen more than 40 per cent from peak levels.

- Housing starts have plunged by more than 60 per cent over several years.

The sector’s unravelling has already produced some of the defining corporate failures of modern China. Major developers such as Evergrande and Country Garden either defaulted or fell into severe distress after years of debt-fuelled expansion.

The broader economic fallout has been severe. Local governments, long dependent on land sales for revenue, have been left with major shortfalls. Construction slowdowns have reduced demand for steel, cement, glass, appliances, and other housing-linked industries. Banks have had to absorb pressure from bad loans and underwater mortgages. Consumers, seeing asset values fall and unfinished projects spread across the country, have become more cautious. That in turn has fed deflationary pressure and weak retail spending.

This is why even a stabilisation story needs to be framed properly. The most likely positive case is not a return to the old growth model. It is a stabilisation at much lower levels of activity, confidence, and contribution to GDP.

China’s earlier era of fast housing growth was not just a sectoral boom. It was one of the core engines of national growth. If that era is over, then a slower China is not a temporary phase. It becomes the new baseline.

For related analysis on the housing downturn and its wider economic effects, see this earlier China update news briefing on property losses and stabilisation risks.

April economic data was worse than expected

If the property data offered a sliver of relief, the rest of the economic picture quickly darkened.

More official data released later in the day showed that China’s economy weakened significantly in April. Fixed asset investment, retail sales, and industrial production all missed expectations, underscoring a persistent problem that Beijing has not solved: domestic demand remains weak.

policymakers weigh what comes next.

The main readings were poor across the board:

- Fixed-asset investment contracted 1.6 per cent in the first four months of 2026 compared with a year earlier.

- Retail sales rose just 0.2 per cent in April, one of the weakest results since the end of COVID restrictions.

- Industrial output grew 4.1 per cent year on year, the weakest pace in nearly three years.

The core issue is not difficult to identify. China can still produce and export. It is struggling to get households and private firms to spend, borrow, and invest with confidence.

Exports have remained relatively resilient. They climbed 15 per cent in the first four months of the year, helped by stronger overseas shipments in technology and AI-related sectors and by a stabilisation in trade ties with the United States after a truce late last year.

But export resilience comes with caveats.

Much of it is supported by state-backed industrial policy and subsidies. That can keep production lines moving, but it does not resolve the underlying weakness in domestic consumption. It can also intensify foreign backlash if trading partners conclude that Chinese industrial overcapacity is distorting global markets.

There are also new pressures building. Rising energy costs linked to the Iran conflict are weighing on manufacturers. Household borrowing slumped again in April, signalling continued caution from consumers after years of property market stress and weaker income growth.

Then there is the labour market, especially for the young.

Youth unemployment has climbed to its highest level in more than two years. That matters not just as a social issue but as an economic one. Young workers and recent graduates are supposed to form part of the consumption base for the next phase of growth. Instead, many are entering a weak job market just as firms begin adopting AI tools that may reduce demand for entry-level white-collar labour.

Put simply, China’s growth model is trying to pivot at the same time that confidence is fragile, property wealth has been damaged, and labour market pressures are rising. That is a difficult combination.

Markets reacted cautiously. The offshore renminbi weakened slightly, and government bond yields were broadly stable, reflecting a sense that more policy support may eventually be needed. If domestic demand keeps deteriorating, Beijing is likely to face stronger calls for additional stimulus.

But even that raises familiar questions. More stimulus can soften the downturn. It cannot easily rebuild household confidence or resurrect the old property-led model.

For a broader look at why the recovery narrative remains fragile, especially amid energy shocks and tech constraints, see this analysis on China’s premature recovery narrative.

US-China trade finds some common ground in agriculture, but frictions remain

Against that weak domestic backdrop, the White House announced a notable development in US-China trade.

China has agreed to purchase at least $17 billion worth of US agricultural products annually through 2028. This was presented as one of the most significant outcomes from President Donald Trump’s recent summit with Xi Jinping in Beijing.

The commitment is in addition to existing soybean purchase agreements reached previously. China had already pledged to buy 25 million metric tonnes of US soybeans each year. The new commitments could extend across products including corn, sorghum, cotton, beef, and poultry.

For the US agricultural sector, this is potentially meaningful. American farmers have been dealing with weak crop prices, elevated fertiliser costs tied to geopolitical tensions, and years of uncertainty in the trade relationship with China. Reports that China has renewed import approvals for more than 400 US beef facilities and is working to restore poultry imports suggest that parts of the farm and food supply chain may get some relief.

Still, scepticism is warranted.

Chinese purchasing pledges made during Trump’s first term were not fully met. That history makes it difficult to treat headline commitments as guaranteed outcomes. Agricultural buying can also be used tactically by Beijing, both as a tool of diplomacy and as a pressure valve in broader trade negotiations.

And even as the two sides announce cooperative steps, the structural trade conflict has not gone away.

The Trump administration is still preparing potential trade actions against China if ongoing US investigations conclude that Chinese industrial overcapacity is unfairly distorting global exports. US Trade Representative Jamieson Greer said officials may present the president with options that could include tariffs, quotas, or service-related fees.

So the picture here is mixed. Agriculture may offer a politically useful area for temporary stabilisation in the bilateral relationship. But that does not mean the wider contest over industrial policy, exports, and strategic technologies is easing.

The two Chinas: stagnation in one economy, rapid technological advance in another

One of the most useful frameworks for understanding China right now is to stop treating it as a single, uniform story.

There are, in practical terms, two Chinas.

The first is the larger one: a country of roughly one billion people moving through a long structural slowdown. This is the China shaped by property contraction, weak consumption, indebted local governments, industrial overcapacity, and shrinking confidence.

The second is smaller but strategically potent: perhaps 50 to 100 million people concentrated in the coastal urban clusters. This is the China with better access to capital, education, infrastructure, elite talent, and state support. China is building advanced manufacturing and pushing forward in EVs, drones, semiconductors, robotics, and AI.

This framework helps resolve an apparent contradiction that often confuses outside observers. China can be facing economic deterioration and still become more formidable in advanced technology. Those two realities can coexist because they are being driven by different segments of the country, with very different resource bases and policy priorities.

The coastal innovation clusters are not representative of the entire national economy. But they are highly consequential. They sit at the intersection of national strategy, industrial policy, and geopolitical competition.

That matters enormously for AI.

Anthropic’s warning: the West could lose its AI lead within two years

One of the more striking developments came from Anthropic, which released a report warning that the United States and its allies could lose their lead in artificial intelligence to China within the next two years unless policymakers move aggressively.

The report, titled 2028: Two Scenarios for Global AI Leadership, frames the issue not simply as a commercial race but as a strategic contest over who shapes the future rules and uses of transformative AI systems.

Anthropic’s core argument is that the decisive battleground is compute, meaning the advanced chips and processing capacity required to train increasingly powerful AI models.

For now, the United States and its allies still hold an important advantage because the most advanced AI chips are largely designed by American and partner firms, especially Nvidia. Export controls on cutting-edge semiconductors have therefore become one of Washington’s most important tools for slowing China’s progress.

Anthropic argues those controls have worked so far, but only partially. Chinese AI firms have reportedly stayed close to the frontier by exploiting loopholes in export restrictions and by using what the company describes as large-scale distillation attacks, methods aimed at extracting capabilities or innovations from leading Western models and reproducing them more cheaply.

The report lays out two broad scenarios for 2028.

Scenario one: the US and allies preserve the lead

In this version, Washington tightens export controls, closes loopholes, limits unauthorised model distillation, and accelerates AI deployment across democratic economies. Anthropic argues that this could preserve a 12 to 24 month lead in frontier capabilities, which it sees as strategically decisive.

Under that outcome, democratic countries would be in a stronger position to shape the norms, governance systems, and safety standards around advanced AI.

Scenario two: China catches up or moves ahead

In the darker scenario, the United States fails to protect its compute advantage or relaxes restrictions too early. Chinese firms then catch up to or surpass American developers, creating a genuine neck-and-neck race.

From Anthropic’s perspective, that would increase the odds that authoritarian governments use advanced AI to strengthen censorship, mass surveillance, cyber operations, and military modernisation while also shaping global standards in their favour.

Whether one agrees fully with Anthropic’s framing or not, the strategic point is clear: AI competition is no longer just about product launches and startup valuations. It is about chips, supply chains, export controls, intellectual property, governance, and national power.

For related context on export controls, AI coordination, and concerns about model distillation, see this China update news report on US AI firms and China-related technology controls.

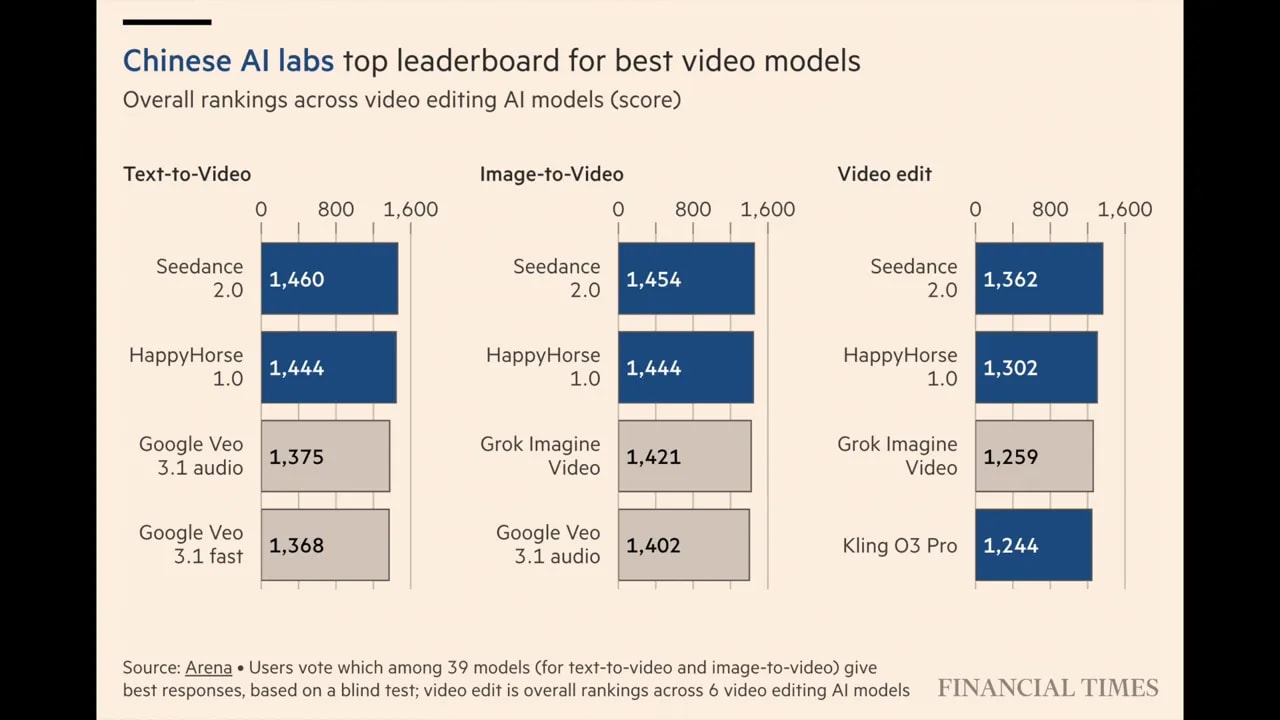

China’s AI video firms are moving fast, and in some areas they may already be ahead

A separate report from the Financial Times adds an important wrinkle to the AI story: Chinese companies are not merely catching up across the board. In AI-powered video generation, some may already be ahead of many US rivals.

Companies including ByteDance, Kuaishou, and startup MiniMax are reportedly gaining an edge in one of the most competitive corners of generative AI. Their advantage appears to come in part from training on enormous libraries of short-form video sourced from platforms such as TikTok and Chinese domestic apps.

Developers and creators cited in that reporting say Chinese models such as Kling, Seedance 2.0, and Hailuo often outperform American systems in several important areas:

- Visual realism

- Prompt accuracy

- Voice stability

- Fast-moving camera scenes

Meanwhile, US firms such as OpenAI and Anthropic continue to dominate in large language models and AI coding tools, but their video generation products are often seen as more restrictive and less flexible.

This is a useful reminder that AI leadership is not monolithic. Strength in one category does not automatically translate into strength in another. China may still lag in some foundational layers, especially advanced semiconductor manufacturing, while competing extremely effectively in application-level products where it has rich data, intense commercial pressure, and fewer content restrictions.

That last point is uncomfortable but important. Looser content controls and aggressive access to training data may be accelerating innovation in some Chinese AI domains, even as concerns over copyright and intellectual property become harder to ignore.

The commercial implications are immediate. Video generation tools are already reshaping advertising, e-commerce, and entertainment by allowing firms to produce large volumes of customised content at a fraction of traditional production cost.

So while the broader Chinese economy is weak, some of its technology champions are operating on a very different trajectory.

The bigger picture

The latest batch of developments points to a China that is becoming more uneven, not less.

The property market may be stabilising, but only after destroying a vast amount of household wealth and undermining one of the country’s core growth engines. April data showed the domestic economy is still struggling, particularly with consumption and investment. Trade with the United States may be finding narrow areas of pragmatism, especially in agriculture, but the deeper structural tensions remain in place.

At the same time, advanced technology sectors continue to move quickly. AI is now central to the geopolitical contest, and China’s progress in areas such as video generation shows that the technology race is more granular and more competitive than simple league tables suggest.

That is the real story right now. Not a clean recovery. Not a clean collapse. But a bifurcated system in which structural stagnation and strategic technological advances are unfolding side by side.

FAQ

Is China’s property crisis over?

No. The latest data suggests that price declines are easing, which may indicate early stabilisation, but prices are still falling and the sector remains deeply damaged. Any recovery is likely to mean stabilisation at much lower levels rather than a return to the old property boom.

Why does China’s economy still look weak if exports are holding up?

Because domestic demand remains fragile. Retail sales, investment, and household borrowing are weak, reflecting low confidence after the property downturn and slower income growth. Exports can support output, but they do not fully offset weak consumption at home.

What did the new US-China agriculture agreement involve?

The White House said China agreed to buy at least $17 billion in US agricultural products annually through 2028, in addition to existing soybean commitments. Products may include corn, sorghum, cotton, beef, and poultry. However, there is scepticism because earlier purchase promises were not fully met.

What does the “two Chinas” idea mean?

It refers to the contrast between a much larger China facing structural slowdown and a smaller, wealthier, more advanced China concentrated in coastal urban clusters that continues to push forward in sectors such as AI, chips, EVs, and drones. Both stories are happening at the same time.

Why is AI competition between the US and China increasingly focused on chips?

Because advanced AI systems require enormous computing power. The most advanced chips are still largely designed by US and allied firms, so export controls on those semiconductors have become a key strategic tool for slowing China’s progress in frontier AI.

Is China leading in any part of AI already?

In AI video generation, Chinese firms appear to be highly competitive and may lead some US rivals in realism, prompt accuracy, and video performance. US firms still dominate in large language models and coding tools, but the race is increasingly segmented by product category.