It has been one of those days where several separate stories all point back to the same underlying reality: China is operating in a far more fragile external environment than many policymakers in Beijing would like.

A relatively limited international disease outbreak is again testing public trust in official health messaging. The AI chip battle between Washington and Beijing is entering another complicated phase, with Nvidia trying to preserve access to China without crossing America’s national security red lines. The war involving Iran is being studied in China not just as a Middle East crisis but as a working demonstration of how future wars could unfold, including any future contingency around Taiwan. And at home, China’s inflation data has turned sharply higher, though for the wrong reasons.

These are very different stories on the surface. But together they show a country still deeply exposed to global shocks through trade, technology, finance, logistics, and confidence.

Table of Contents

- China moves to calm concerns over the hantavirus outbreak

- Nvidia wants to keep China, but not give it America’s best chips

- China is treating the Iran war as a live lab for future conflict

- Beijing’s Iran dilemma: strategic partner, unstable oil market

- China’s inflation surprise is not the kind policymakers wanted

- The bigger picture

- FAQ

China moves to calm concerns over the hantavirus outbreak

Chinese health authorities spent the weekend trying to reassure the public that the recent hantavirus outbreak linked to a cruise ship does not present a meaningful domestic threat. The outbreak, tied to the Andes strain, triggered an international health response after at least three deaths and a number of potential exposures involving passengers from more than 20 countries.

The ship departed Argentina in early April, and infections later emerged among passengers and crew. The World Health Organization has stressed that the overall public health risk remains low. Still, the story has drawn outsized attention in and around China because public sensitivity to disease management remains extremely high in the post-COVID era.

China’s CDC was quick to emphasise several key points:

- There have been no domestic human infections linked to the current outbreak.

- The Andes strain is the only known hantavirus variant capable of limited human-to-human transmission.

- This strain does not have a natural host population in China.

- Hantavirus generally does not spread through normal social interaction.

- The risk of widespread transmission remains very low.

On the narrow public health facts, that is reassuring. But this story is not only about epidemiology. It is also about trust.

Even when the objective risk is low, Chinese official messaging on disease outbreaks is now filtered through the memory of Wuhan in late 2019, when local authorities were criticised for delayed disclosures, information suppression, and the silencing of medical whistleblowers during the critical opening phase of the COVID crisis.

That legacy matters. It means even a contained outbreak can trigger speculation, suspicion, and accusations of concealment very quickly. Sometimes that scrutiny is warranted. Sometimes it is not. But politically, the burden of proof is now much heavier than it once was.

For Beijing, this creates a difficult balancing act. Authorities want to avoid panic, economic disruption, and another blow to already weak consumer sentiment. At the same time, any sign of opacity can erode confidence even faster than the outbreak itself.

The situation also underlines a broader truth. China may have strict domestic controls, but it remains tightly integrated into global tourism, transport, and trade networks. Imported health risks cannot be wished away. Monitoring at airports, ports, and transport hubs is likely to intensify. That would be unsurprising in the current environment.

The political timing is awkward as well. Beijing has spent years trying to rebuild international credibility after both the initial COVID fallout and the later zero-COVID lockdown period. Another health scare, even one that originated outside China, risks reopening old arguments over transparency and preparedness.

The important distinction here is that hantavirus is not COVID-19. Transmission is far more limited, and there is no indication that this outbreak could trigger a global pandemic. But in the post-COVID world, even small outbreaks can become geopolitical events.

For more on how governance concerns and disease reporting have become global market issues, there is some useful related context in this earlier China update news analysis.

Nvidia wants to keep China, but not give it America’s best chips

The next major story sits at the heart of the US-China tech confrontation.

Nvidia CEO Jensen Huang has argued that China should not receive America’s most advanced AI chips, but US semiconductor companies should still be allowed to compete aggressively in the Chinese market. Speaking at the Milken Institute Global Conference in Los Angeles, Huang framed the issue as one of long-term American advantage, not concession.

His core argument is straightforward: US leadership in artificial intelligence depends not only on superior technology, but also on continued access to global markets. American technology companies, he said, strengthen US national and economic security through exports, taxes, and dominance in the defining industrial race of the era.

Huang’s line was clear. The United States should have “the first, the most, and the best". But shutting US firms out of China entirely, in his view, would damage America’s long-run competitiveness.

This is where the policy tension becomes acute. Washington has continued tightening export controls on advanced semiconductor technology as AI becomes increasingly entangled with national security planning. Nvidia’s latest Blackwell chips and upcoming Rubin systems remain restricted in China. Yet the company recently received approval to export H200 processors to approved Chinese customers.

That is significant because the H200 is meaningfully more powerful than the H20 chips Nvidia previously tailored to comply with earlier rounds of export restrictions. Huang has said demand from Chinese buyers is already strong.

Critics in the United States are not persuaded. Their concern is blunt: if Nvidia sells powerful chips into China, then Chinese firms can use those chips to build AI systems that may one day be directed against American interests. Huang has pushed back hard against that line of attack, arguing that widespread adoption of American technology helps cement US leadership rather than weaken it.

Beijing, meanwhile, is not a passive participant in this story. Chinese authorities are reportedly considering new rules governing Nvidia chip imports as they try to support domestic semiconductor development while also meeting local demand for high-end AI hardware. That is a difficult balance because China wants self-reliance, but Chinese firms still need advanced compute now.

This issue may also feed into broader trade discussions during the expected Trump-Xi talks in Beijing. There is even speculation that Huang could be part of a wider US business delegation. If so, it would underline how central AI chips have become to the larger US-China relationship.

At the market level, the AI theme is clearly energising Chinese technology stocks. Mainland tech shares surged after reopening from the holiday break, with the STAR 50 index jumping sharply and briefly climbing more than 9 per cent intraday before settling near record levels. Semiconductor names and AI hardware firms led the gains.

The rally reflects two things at once:

- Renewed optimism around global AI demand

- Improved sentiment toward China’s domestic semiconductor ecosystem

That said, investors should be careful not to confuse a market rally with strategic resolution. China’s domestic tech sector has made progress, but the advanced chip bottleneck is still real. The broader picture remains one of constrained access, policy uncertainty, and intense geopolitical competition. That theme is explored further in this China update news piece on China’s fragile recovery and AI chip constraints.

China is treating the Iran war as a live lab for future conflict

One of the most consequential stories now unfolding is not economic at all, at least not initially. Chinese military strategists are increasingly studying the war involving Iran as a real-time test case for modern warfare and, by extension, as a source of lessons for any future crisis involving Taiwan.

For Beijing, this is not simply a distant regional conflict. It is a dense package of military, economic, diplomatic, and logistical lessons.

Chinese analysts are paying close attention to several questions:

- How does the United States perform under sustained military and economic pressure?

- How effective are high-end missile defence systems against large numbers of cheap drones and missiles?

- How quickly can a regional war spill over into global commodity, shipping, and energy markets?

- What matters more in a prolonged conflict: offensive strike power or resilience and logistics?

A growing view among Chinese and Taiwanese observers is that the war has reinforced a sobering lesson for all militaries: technological superiority does not automatically produce decisive political results.

That matters because one of the most closely studied features of the conflict has been the ability of relatively inexpensive Iranian drones and missiles to penetrate sophisticated US and allied defences. Systems such as Patriot and THAAD are formidable, but they are not magical. Scale, cost asymmetry, and saturation matter.

That resonates strongly in Beijing because China has spent years building capabilities in exactly these areas, including hypersonic missiles, long-range precision strike systems, stealth aircraft, and advanced naval assets. China is also developing a new strategic stealth bomber, widely seen as conceptually comparable to America’s B-2 and B-21 approach.

But the Iran conflict appears to be sharpening a more mature lesson inside Chinese strategic circles: offensive systems alone are not enough. In a prolonged war, hardened infrastructure, supply redundancy, logistics, domestic resilience, and the ability to absorb punishment may prove just as important as flashy strike capability.

Why Taiwan sits at the center of these lessons

Nowhere are these lessons more relevant than the Taiwan Strait.

Taiwanese defence analysts increasingly expect that any future Chinese campaign would involve a blend of precision missile strikes, cyber warfare, and large drone swarms intended to overwhelm defences by sheer volume. China’s dominance in global drone manufacturing only deepens those concerns. In wartime, civilian production lines could potentially be shifted toward military output, enabling enormous numbers of low-cost unmanned systems.

Taiwan has acknowledged weaknesses in counter-drone capacity and is accelerating investment in domestic drone production, electronic warfare, and air defence systems. US Indo-Pacific Commander Admiral Samuel Paparo has also argued that thousands of drones could one day saturate the strait itself, targeting Chinese ships and aircraft during any attempted amphibious assault.

There is another issue, however, that may be even more important than platforms and hardware: combat experience.

The People’s Liberation Army has not fought a major war since the short 1979 conflict with Vietnam. US forces, by contrast, have accumulated decades of operational experience across Iraq, Afghanistan, and the wider Middle East. That does not guarantee success in every future conflict, but it does mean the US military has spent years adapting under real battlefield pressure.

Military observers note that American forces in the current Iran-related conflict continue to adjust tactics, reposition assets, harden vulnerable areas, integrate allied support, and combine direct military pressure with naval and economic tools. Whether the PLA could adapt with similar speed under combat conditions remains an open question, especially given recent military purges near the top of China’s command system.

Beijing’s Iran dilemma: strategic partner, unstable oil market

China’s diplomatic posture reflects a deeper contradiction.

Beijing has close economic and diplomatic ties with Tehran. At the same time, China depends heavily on stability in Middle Eastern energy markets and wants to avoid direct confrontation with Washington, especially ahead of high-stakes top-level talks.

At the United Nations, the United States has pushed for a resolution demanding Iran halt attacks and mining operations in the Strait of Hormuz. China and Russia are widely expected to oppose or veto such a measure. Beijing has condemned attacks on energy infrastructure in the UAE while warning against wider escalation.

This balancing act is getting harder. The broader US-China discussion is now expected to include allegations that Chinese firms supplied dual-use technology, satellite imagery, and weapons-related components to Tehran. The Trump administration has already sanctioned several Chinese companies accused of aiding Iran’s military operations.

And yet, despite the geopolitical tension, both sides are still trying to stabilise the wider bilateral economic relationship through talks on agriculture, aerospace, AI, and investment frameworks.

The larger strategic lesson for Beijing is uncomfortable but clear: in an interconnected global economy, modern wars do not stay on the battlefield. They hit shipping lanes, insurance costs, fuel prices, supply chains, and diplomatic alignments. Even countries that are not directly fighting can take serious economic damage.

That broader Hormuz and energy-security angle has been developing for some time. A useful companion read is this China update news article on Hormuz turmoil, producer inflation, and Taiwan blockade planning.

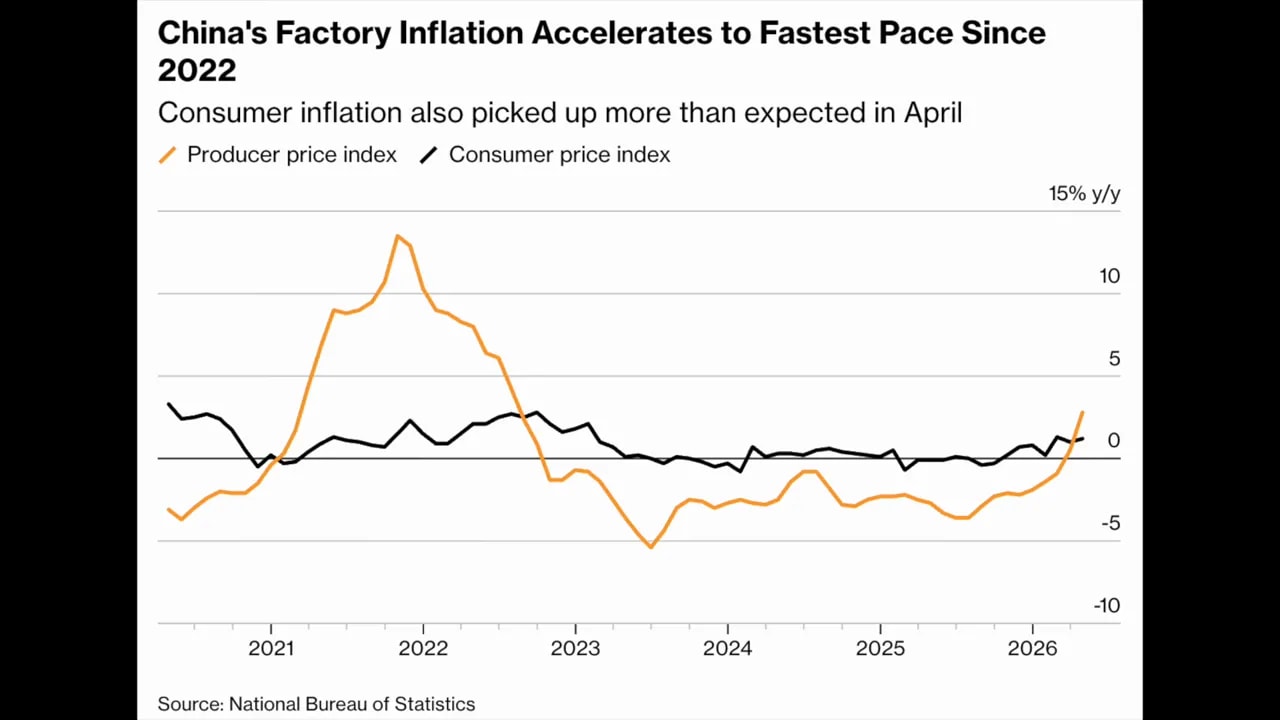

China’s inflation surprise is not the kind policymakers wanted

The final major development is economic, and it is significant.

China’s factory inflation accelerated sharply in April, with the producer price index rising 2.8 per cent year on year, up from 0.8 per cent in March and well above expectations. It was the strongest increase since July 2022. Consumer inflation also surprised modestly to the upside, with CPI rising 1.2 per cent from a year earlier compared with 1 per cent in March.

At first glance, after a long stretch of deflationary pressure, a rebound in inflation might sound like welcome news. It is not that simple.

Financial markets initially treated the data as meaningful. The renminbi strengthened against the US dollar, briefly moving past the psychologically important 6.8 level, while long-dated Chinese government bond futures fell as investors reassessed inflation risk.

But the composition of the inflation matters more than the headline. Chinese officials attributed the rise in producer prices to soaring global commodity costs, stronger demand in some domestic sectors, and changing market conditions. The biggest driver, however, appears to be the war-linked shock in energy and shipping markets.

Industries most exposed to energy and raw materials saw the largest price increases, including:

- Crude oil extraction

- Petroleum processing

- Chemicals

- Non-ferrous metals

- Electronics and electrical machinery

That means this is not the healthy sort of inflation that signals stronger household demand, rising confidence, and better corporate pricing power. It is cost-push inflation.

And that is a very different story.

Domestic demand in China remains weak. Labour market conditions are still soft. Consumers are cautious. Firms in many sectors remain locked in fierce price competition due to overcapacity. So when input costs rise, many companies cannot fully pass those costs on to customers. Instead, margins get squeezed further.

That is the real problem. China may be emerging from factory-gate deflation statistically, but many of the structural forces that created the deflationary environment are still there:

- Weak consumption

- Overcapacity in major industrial sectors

- Intense price competition

- Soft labor market conditions

- Limited ability for firms to raise final selling prices

So this inflation rebound is not evidence that the growth model has healed. In many respects, it simply adds another layer of strain. Costs are going up, but profitability is not necessarily improving. For manufacturers and service providers already operating on thin margins, that is a serious problem.

This is also why Beijing’s policy challenge is becoming more difficult. If inflation is being pushed up by imported energy and commodity shocks rather than strong domestic recovery, then policymakers have less room to celebrate and fewer clean tools to solve it. Stimulus can help demand at the margin, but it cannot directly remove the external supply shock. And if officials lean too hard on credit expansion without fixing the structural imbalance, they risk worsening the underlying overcapacity problem.

The bigger picture

Put all of these stories together and a consistent picture emerges.

China is still highly vulnerable to external shocks, even when those shocks begin far beyond its borders. A cruise ship outbreak in South America becomes a domestic credibility issue. US export controls on AI chips become a strategic constraint on China’s technology ambitions. War in the Middle East becomes a military case study, a diplomatic headache, and an inflation problem all at once.

That is the environment Beijing now has to manage: one where trust is brittle, supply chains are political, markets react instantly, and every crisis has multiple layers.

There is no single master narrative that neatly explains everything. But there is a clear pattern. China’s leadership is trying to preserve stability while navigating a world in which health security, national security, economic security, and technological security increasingly overlap.

That overlap is exactly why these developments matter far beyond their individual headlines.

FAQ...

Is the current hantavirus outbreak a major threat to China?

At this stage, Chinese authorities and international health officials say the risk is very low. The Andes strain linked to the outbreak is not believed to have a natural host population in China, and no domestic human infections connected to the outbreak have been reported.

Why has the hantavirus story received so much attention in China?

Because public trust in disease reporting remains shaped by the early COVID period. Even relatively limited outbreaks now receive much closer scrutiny, both inside China and internationally, due to concerns about transparency and crisis management.

What is Jensen Huang’s position on selling AI chips to China?

He argues that China should not receive America’s most advanced chips, but US companies should still be allowed to compete in the Chinese market. His view is that maintaining US technological dominance also requires access to major global customers.

Why is the Iran war important to Chinese military planners?

Chinese strategists see it as a real-world demonstration of modern warfare. They are studying missile defence performance, drone saturation tactics, economic disruption, logistics, and how technologically advanced militaries cope with prolonged pressure. Many of those lessons are relevant to Taiwan planning.

Is China’s recent inflation rebound a sign of stronger recovery?

Not necessarily. The rise in producer prices appears to be driven mainly by higher commodity and energy costs linked to the Middle East conflict. That means it is more of a cost shock than a demand-led recovery, and it may further squeeze company profit margins.

Why does overcapacity matter in China’s inflation story?

Because many firms are still competing aggressively in oversupplied sectors and cannot easily pass higher costs on to customers. Even if input prices rise, final selling prices may not rise enough to protect margins, which keeps financial pressure on producers.