China update news this week points to a sharper sense of strain across the Chinese economy and policy landscape. Three developments stand out. First, the war in Iran is pressuring China through energy markets, manufacturing costs, weak consumption, and rising risks around sanctions. Second, Beijing has unveiled a new framework for protecting gig workers, signaling that precarious platform labor is no longer a side issue but a core feature of the labor market. Third, Chinese regulators have forced Meta to unwind its acquisition of the AI startup Manus, underscoring how far Beijing’s national security reach now extends in cross-border technology deals.

Taken together, these stories reveal a broader pattern. China is still capable of using state tools to cushion shocks, but those tools are being tested by deeper structural weaknesses: soft domestic demand, reliance on manufacturing, fragile employment, and growing geopolitical friction.

Table of Contents

- China’s economy is absorbing an external shock that exposes older internal problems

- Car sales are falling hard, and that matters far beyond the auto sector

- Consumption remains fragile despite policy support

- Factories are building inventories instead of shipping goods

- Labor unrest in southern China highlights stress in low-margin industries

- China’s energy buffers are helping, but they come with limits

- The sanctions risk around Iranian oil is growing

- Why the biggest risk is stagflation, not just slower growth

- Beijing moves to formalize the gig economy

- Algorithmic management has become a policy target

- Why gig work is expanding as traditional employment weakens

- The Meta-Manus case shows how cross-border tech deals have changed

- Why Beijing’s order matters beyond one company

- Due diligence appears to have been a major weakness

- A warning shot for foreign capital

China’s economy is absorbing an external shock that exposes older internal problems

For years, China was often described as better insulated than many major economies from sudden external disruptions. It had large policy buffers, strong state control over finance and pricing, and the ability to mobilize strategic reserves. That resilience has not disappeared, but the current energy shock tied to the Iran war is showing its limits.

At the center of the problem is a familiar economic squeeze. Oil and gas prices are rising, which lifts input costs across transport, manufacturing, and logistics. At the same time, domestic demand inside China remains weak. That combination is especially difficult because companies face higher costs while consumers are less willing or less able to spend.

This is not simply an energy story. It is an economic stress test.

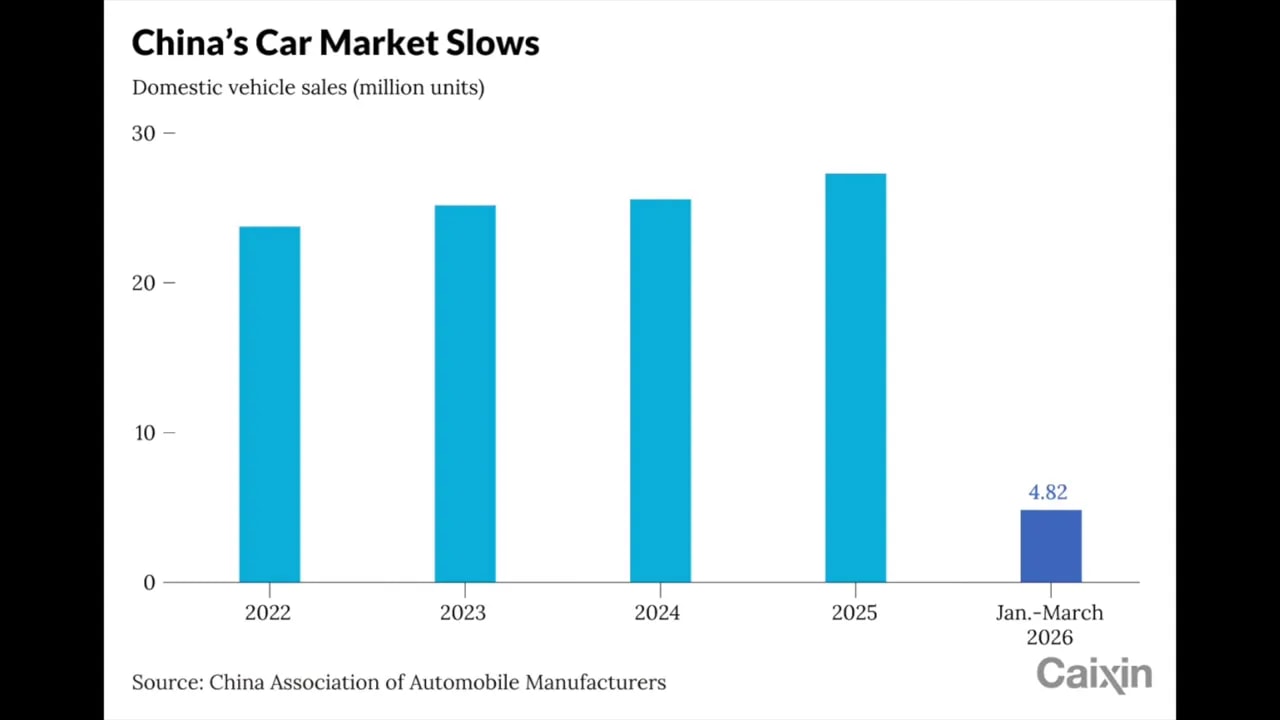

Car sales are falling hard, and that matters far beyond the auto sector

One of the clearest warning signs is the sharp decline in vehicle sales. Early April retail car sales fell 26 percent from a year earlier, while gasoline vehicle sales dropped 40 percent. Those are severe contractions in a sector that remains a central pillar of China’s industrial economy.

The weakness is not limited to traditional automakers. BYD, one of China’s best-known electric vehicle champions, reported first-quarter net profit of 4.1 billion RMB, roughly 600 million US dollars, down 55 percent year over year. Only part of that quarter overlapped with the Iran conflict, which suggests the pressure cannot be explained by geopolitics alone.

Other domestic issues are clearly in play, including:

Overproduction in electric vehicles

Weak household demand

Competitive pressure on margins

The importance of this slowdown goes well beyond car dealerships. Auto manufacturing drives demand for steel, glass, electronics, batteries, and a wide network of suppliers. Falling vehicle sales can quickly translate into lower factory utilization, production cuts, and reduced orders across related industries.

Consumption remains fragile despite policy support

Retail sales growth slowed to just 1.7 percent in March, even against a relatively weak comparison base. Restaurants and hotels are also reporting weaker traffic. That points to a deeper confidence problem in Chinese households.

Several constraints continue to weigh on consumption:

A weak property market that has reduced household wealth and confidence

Uncertain income prospects as layoffs and soft labor conditions persist

Higher energy-related costs that reduce discretionary spending

When households grow more cautious, the effects spread quickly. Less spending means weaker demand for services, fewer durable goods purchases, and slower turnover of inventories. That becomes especially dangerous when production has already been built around higher growth assumptions.

Factories are building inventories instead of shipping goods

On the industrial side, inventory accumulation is becoming a clear warning signal. Rising inventories usually mean producers are making more than markets are absorbing. In China’s case, that appears to be happening on both fronts: domestic buyers are hesitant, and external demand is under pressure as well.

That creates a difficult cycle. If goods do not move, firms eventually cut production. If production falls, they may reduce hiring, wages, or working hours. Those adjustments then feed back into weaker consumption.

The pressure is particularly intense in low-margin export manufacturing, where even modest cost increases can push firms into shutdown territory.

Labor unrest in southern China highlights stress in low-margin industries

Southern China has already seen signs of labor tension. Thousands of toy factory workers recently protested after factory closures linked to two overlapping pressures: rising plastic costs associated with higher oil prices and ongoing US tariffs.

This is a revealing example because it shows how external demand weakness and rising input costs can collide in sectors with very little room for error. Toy manufacturing is highly competitive and often operates on thin margins. When raw material costs rise and export conditions worsen, many factories cannot absorb the hit.

The broader concern is social stability. If shutdowns spread from toys into other light manufacturing sectors, unemployment could rise in places that depend heavily on factory work. Beijing has long treated employment as an economic and political priority. Protests in one industry may be manageable, but a wider pattern would pose a more serious challenge.

China’s energy buffers are helping, but they come with limits

So far, the Chinese state has used several tools to cushion the energy shock. Authorities have drawn on stockpiles, limited the pass-through of global oil price increases to domestic consumers, and directed state-owned firms such as Sinopec and China National Petroleum Corporation to prioritize local supply over exports.

These measures can buy time, but they are not cost-free.

Suppressing fuel price increases can distort market signals and delay adjustment

Restricting exports can worsen shortages elsewhere and create diplomatic friction

Using reserves helps in the short term but does not solve prolonged supply pressure

In other words, state management can soften the immediate blow, but the longer the conflict lasts, the harder it becomes to avoid trade-offs.

The sanctions risk around Iranian oil is growing

The geopolitical dimension may become even more important than the direct energy shock. The United States has stepped up enforcement efforts around Iranian oil flows, with the US Treasury warning of sanctions on Chinese refiners involved in processing Iranian crude.

This matters because China is estimated to import about 90 percent of Iran’s oil exports. If sanctions enforcement intensifies, Chinese firms could face disruptions not only in crude supply but also in shipping, payments, insurance, and financial settlement channels.

If access to discounted Iranian oil narrows, China would likely need to compete more aggressively on global markets at higher prices. That would remove one of the advantages it has relied on during periods of external energy stress.

Why the biggest risk is stagflation, not just slower growth

The most serious macroeconomic threat is not simply weaker growth. It is a stagflation-like environment, where costs rise while demand remains soft.

That combination can be especially damaging because it squeezes nearly every part of the economy at once:

Corporate margins fall as input prices climb

Investment weakens because expected returns deteriorate

Household consumption softens further under financial pressure

Employment risks increase as firms reduce output

China’s deeper structural vulnerability is that it still relies heavily on manufacturing and exports at a time when both are under strain. If domestic consumption does not recover meaningfully, and external demand remains weak, the economy could face a more persistent slowdown rather than a short-lived dip.

Beijing moves to formalize the gig economy

The second major development in China update news concerns labor policy. Beijing has introduced a 12-point framework aimed at strengthening protections for more than 200 million gig workers, who now account for over a quarter of China’s labor force.

This is a significant policy signal. Informal and platform-based work in China is no longer being treated as temporary or peripheral. It is now being acknowledged as a structural part of the labor market.

The plan, issued jointly by the State Council and the Communist Party’s Central Committee, promises improvements in several areas:

Timely wage payments

Expanded social security coverage

Stronger protection during extreme weather

Greater transparency in algorithmic management

Limits on excessive platform price competition

Algorithmic management has become a policy target

One of the most notable parts of the new framework is its focus on platform algorithms. Chinese gig workers, especially in delivery and ride-hailing, have long complained about opaque systems that determine order allocation, pricing, deadlines, and penalties.

Those systems often shape real earnings more than headline pay rates do. A worker may appear to have flexibility, but if the platform controls the timing, route pressure, and incentive structure through algorithms, the worker’s bargaining power can be very limited.

By pushing for more transparency in how orders are assigned and how time limits are imposed, authorities are signaling concern not only about labor conditions but also about fairness and social stability.

Why gig work is expanding as traditional employment weakens

The timing of these reforms is important. China’s labor market is under strain. Youth unemployment remains elevated, and job losses across property, manufacturing, and other sectors have pushed more workers into flexible but insecure gig roles.

That shift has major economic implications. Gig work can absorb labor quickly, but it often offers low and volatile income. That makes it difficult for households to spend confidently, save predictably, or plan for the future.

Beijing says it wants labor practices across the platform economy standardized by 2027. But formalizing this sector will not be simple. Better protections will likely raise costs for technology platforms, reduce margins, and possibly change pricing for consumers.

The harder issue is whether reforms can materially lift incomes rather than simply improve compliance on paper.

Given the sheer number of people in delivery and ride hailing, a serious plan to raise wages and create a stronger social security system in the gig economy is exactly what China would need to raise the consumption share of GDP.

That observation captures the logic behind the policy. If workers have steadier incomes and stronger protections, consumption could improve. But there is an obvious funding problem. Meaningful reform requires money, and that money must come from somewhere, whether through more debt, lower subsidies elsewhere, or reduced investment spending.

The Meta-Manus case shows how cross-border tech deals have changed

The third major story involves technology regulation and foreign investment. Meta is reportedly preparing to unwind its 2.5 billion US dollar acquisition of Manus after Chinese authorities blocked the deal.

The case is rapidly becoming a benchmark for how difficult China-linked technology deals have become, especially when artificial intelligence and national security concerns intersect.

Meta had acquired Manus, a Singapore-based but China-linked AI startup specializing in autonomous agents, and had already integrated its technology into core systems. Reversing that acquisition is not a simple legal formality. It involves disentangling technology, reversing data transfers, and potentially reassigning personnel and intellectual property.

Why Beijing’s order matters beyond one company

Chinese authorities reportedly gave Meta only weeks to fully unwind the deal, restore Manus’s Chinese assets to their original state, and remove transferred intellectual property. Penalties remain possible if the reversal is incomplete.

The immediate implication is that Beijing appears willing to assert authority over a company incorporated outside mainland China if the business still has deep operational ties to the mainland. That is a major point for global investors, because it narrows the value of paper restructurings or offshore domiciles as shields from Chinese oversight.

Several broader lessons stand out:

Chinese regulatory veto power can extend beyond its borders when national security is invoked

Technology deals involving China-linked assets now require much more rigorous due diligence

Cross-border investment structures are becoming more segmented as firms separate politically sensitive capital and operations

Due diligence appears to have been a major weakness

Reports indicate that Meta conducted only a few weeks of due diligence and did not seek Chinese regulatory approval for either the acquisition or Manus’s relocation to Singapore. In a tightening environment around AI and data-sensitive sectors, that omission is striking.

Legal and market participants increasingly view this case as a turning point. The old assumption that shifting incorporation offshore could reduce political risk is becoming less reliable if the underlying business still has mainland staff, research, data, or operational dependence.

As a result, investors are likely to insist on cleaner separation measures in future deals, including:

Clearer ownership structures

Relocated research and development

Stronger intellectual property controls

Explicit review of Chinese national security exposure

A warning shot for foreign capital

The Manus episode also carries a wider market message. Investors and law firms have described the decision as a milestone in the long-arm application of China’s national security review regime. In practical terms, companies may now start treating Beijing review as a