China update news is being shaped by three developments with unusually large consequences for Asia and the global economy. China’s housing market may be showing early signs of stabilization after years of decline, but the damage already done is immense. At the same time, Beijing is pushing ahead with one of the biggest electricity expansions in modern history, raising both strategic hopes and financial risks. Meanwhile, Taiwan is emerging as a major winner from the artificial intelligence boom, with chip demand driving growth, investment, and geopolitical relevance.

These are not isolated stories. Together, they show how the economic balance in the region is shifting. China is trying to manage the fallout from a collapsed property model while investing heavily in the infrastructure of future industry. Taiwan, by contrast, is benefiting from a global technology cycle that is boosting exports, lifting markets, and reinforcing its strategic importance.

Table of Contents

- China housing news: signs of stabilization, but no real escape from the crisis

- China energy news: a power expansion on a historic scale

- Taiwan economy news: the AI boom is transforming growth, markets, and strategy

- What these three stories say about the regional economy

- FAQ

China housing news: signs of stabilization, but no real escape from the crisis

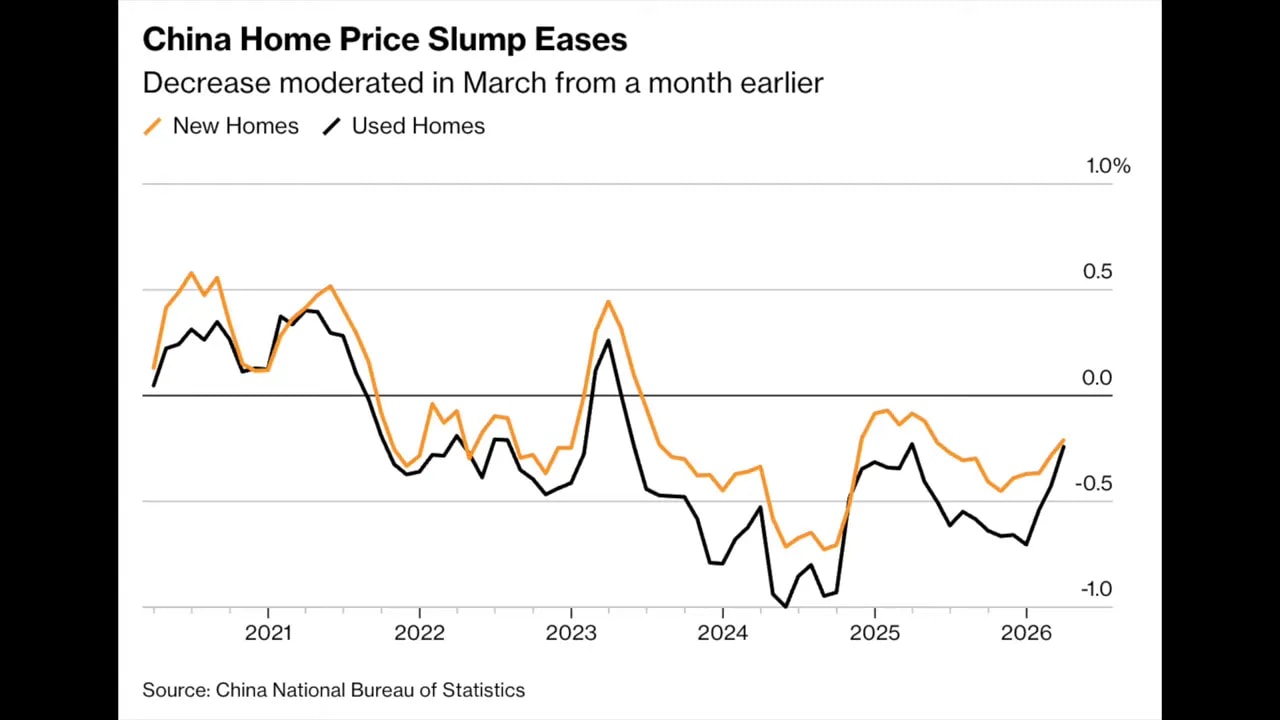

China’s property market has been in decline for years, and recent data suggests the pace of deterioration may be easing. That matters because housing has long been one of the most important pillars of China’s growth model, household wealth, and local government finance.

Official data from the National Bureau of Statistics indicated that new home prices across 70 cities fell 0.21% in March. That marked the second straight month in which declines became less severe, and it was the smallest monthly drop in nearly a year. Resale home prices also improved, declining 0.24%, the mildest contraction in about twelve months.

Those numbers do not indicate recovery. They indicate a slower rate of decline. Even so, in a market that has been under sustained pressure, moderation is significant.

Why prices may be falling more slowly

Local governments have rolled out targeted measures to support demand. These efforts include:

Easing home purchase restrictions

Reducing transaction taxes

Allowing more non-residents to buy in large cities such as Shanghai

Lowering the tax burden on properties sold after shorter holding periods

These policy changes appear to be having the greatest effect in the secondary market, especially in larger urban centers where demand fundamentals are relatively stronger.

In March, used home prices rose in 13 cities, the highest number in nearly three years. Beijing was among the leaders, with modest gains in existing home values after previous rounds of policy support. This has encouraged the view that top-tier cities may lead any eventual recovery.

Why the national picture is still much worse than the headline suggests

The core problem is that China does not have one unified housing market. It has many local property markets with very different conditions.

Some major cities still have high incomes, population inflows, and debt burdens that may be heavy but manageable. These areas could approach a bottom sooner. But much of the country faces weaker demographics, slower income growth, and far more severe local government financial stress.

That makes any national average potentially misleading. A handful of stronger cities can lift the overall figures while large parts of the country remain stuck in prolonged decline.

Analysts point to new data raising hopes that the long, beleaguered housing market may finally be nearing a bottom. But it is not helpful to look at the Chinese property market as a single market.

That caution captures the central issue. In China’s strongest regions, stabilization may be possible. Elsewhere, the downturn may still have years to run.

The wealth destruction is enormous

The deeper story is not just about home prices. It is about balance sheets. China’s property downturn, now in its fifth year, has erased an estimated $18 trillion in household wealth.

This scale is possible because real estate occupied an unusually dominant place in household finances. At the height of the housing bubble, property accounted for roughly 90% of household wealth in China. Even after the decline, it still represents around 70%.

That concentration means even relatively small price moves have very large effects. A 5% drop in home prices can destroy roughly $2.7 trillion in wealth. That is an extraordinary figure and helps explain why the property slump has depressed consumer confidence so deeply.

In many parts of the country, home values have fallen enough to leave households in negative equity, where the mortgage is larger than the home’s market value. Estimates suggest that millions of homes could remain underwater in the years ahead, with one estimate placing the figure at 3 to 4 million.

The consequences go beyond homeowners:

Consumption weakens because households feel poorer and become more cautious.

Deflationary pressure rises as weak demand weighs on prices across the economy.

Local governments suffer because land sales were a major source of revenue.

Banks and developers remain exposed through bad loans and unfinished projects.

Can China finally reach a bottom?

Some analysts believe selected cities such as Shanghai and Shenzhen could bottom by late 2026, with weaker regions following later. Others remain much more pessimistic, arguing that entrenched expectations of falling prices, unresolved bad debt, and the absence of a decisive national policy solution will keep the sector under pressure for years.

The most realistic reading is that China’s housing market may be entering a new phase, but not necessarily a clean recovery. A slower decline in top cities is very different from a nationwide rebound.

For the broader economy, the central fact remains unchanged: the property model that once powered high growth has been broken. Whether the next stage is gradual stabilization or another leg down, the old era is over.

China energy news: a power expansion on a historic scale

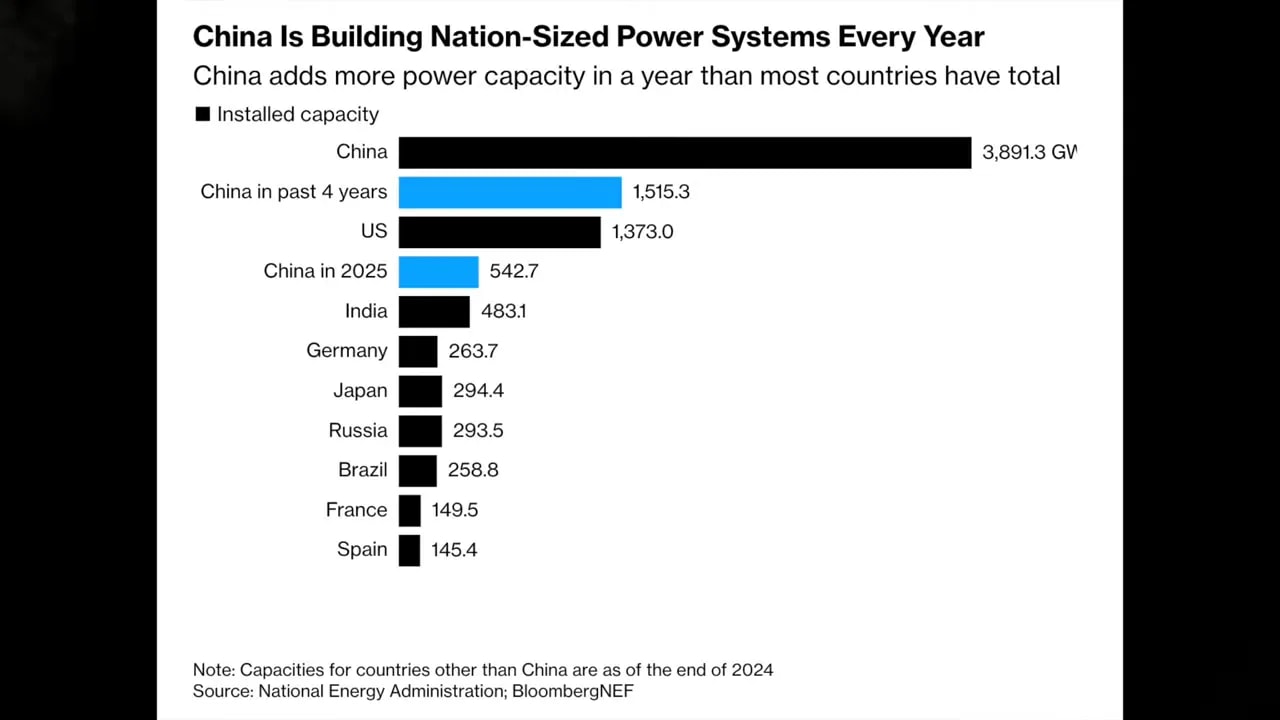

The second major story in China update news is Beijing’s extraordinary electricity buildout. China is adding power capacity at a pace that rivals entire national grids.

According to the National Energy Administration, the country added 543 gigawatts of new power capacity in 2025 alone. That is more than the total installed capacity of countries such as India. Since the end of 2021, the amount of capacity China has added exceeds the entire power system of the United States.

This is not just a construction story. It is a strategic industrial policy. Beijing wants energy security, lower dependence on imports, and abundant electricity to support the next wave of heavy technology industries.

Why China is building so much power

Electricity demand is tied to China’s future growth strategy. Sectors such as artificial intelligence, robotics, advanced materials, and high-end manufacturing are all energy intensive. Reliable and low-cost power is increasingly seen as a competitive advantage.

China also wants to avoid the kind of bottlenecks now emerging elsewhere. In the United States, electricity demand is rising again after decades of stagnation, largely due to data centers and AI workloads. That has tightened supply in some regions. China appears to be trying to build ahead of demand.

An all-of-the-above strategy

What makes the Chinese approach notable is that Beijing is not choosing between renewables and dispatchable generation. It is pursuing both.

New additions in 2025 included:

315 GW of solar

119 GW of wind

95 GW of thermal power, mainly coal and natural gas

Smaller but important increases in hydropower and nuclear

That combination reflects a dual objective. China wants to scale cleaner energy rapidly while keeping enough stable generation online to maintain grid reliability.

The policy shift was reinforced by the power shortages of 2021 and 2022, which exposed vulnerabilities in the system. Since 2023, annual additions have averaged more than 400 GW, almost triple the pace of the previous decade.

The risks: overcapacity, underutilization, and debt

Scale alone does not guarantee efficiency. China’s power system is now expanding faster than it can always absorb. In some areas, rapid growth in wind and solar has outpaced transmission capacity, leading to curtailment, where available electricity cannot be fully used.

There are also growing contradictions:

Coal plants continue to be built

Renewable generation is rising quickly

Thermal plant utilization rates are falling

Debt continues to accumulate through state-backed lending

This raises an uncomfortable question. Is China building a future-proof energy system, or is it also building another layer of overcapacity that will generate weak returns?

Much of the financing comes through local governments and state-owned enterprises, which are already burdened by heavy debt. If assets sit idle or earn poor returns, the cost does not disappear. It shifts into the financial system and adds pressure to an economy already struggling with diminishing returns on investment.

Another complication is that not all capacity is equal. A gigawatt of solar does not generate the same annual output as a gigawatt of nuclear power because solar is intermittent. That reality is one reason China is also pushing hard into nuclear energy.

Nuclear as the stability layer

China currently operates around 60 reactors and has 36 more under construction, the largest pipeline in the world. Plans call for nuclear capacity to reach 110 GW by 2030, a roughly 76% increase.

This matters because nuclear offers stable, around-the-clock power without the intermittency of wind and solar. In strategic terms, it fits Beijing’s desire for secure industrial electricity as manufacturing becomes more automated and more digitally intensive.

Even the solar boom has a profitability problem

One of the most striking tensions is that while solar capacity is exploding, many of the companies producing the equipment are suffering from collapsing profits. Overcapacity and fierce price competition have pushed much of the sector into losses, despite state support.

That concern became more visible when agencies including the Ministry of Industry and Information Technology and the National Development and Reform Commission called for stronger capacity controls in solar. Authorities have met multiple times this year with solar manufacturers that are struggling under excess supply.

The message is clear: rapid expansion can be strategically impressive and economically problematic at the same time.

If large portions of the new power system do not generate adequate economic output, the result could be weaker productivity, rising debt-servicing costs, and additional pressure on financial stability. China may be trying to build the electrical foundation for its next industrial era, but it is doing so while carrying the liabilities of the previous one.

Taiwan economy news: the AI boom is transforming growth, markets, and strategy

While China wrestles with property losses and investment efficiency, Taiwan is benefiting from one of the strongest global technology trends in years. The AI boom is reshaping Taiwan’s economy and strengthening its place in the international system.

At the center of this transformation is Taiwan Semiconductor Manufacturing Company, or TSMC. Its advanced chipmaking capabilities have made it indispensable to major AI developers and technology firms, including Nvidia, Apple, and large cloud providers.

Why AI demand matters so much for Taiwan

As AI systems become more powerful, the need for cutting-edge semiconductors has surged. Demand is especially strong for the most advanced process nodes, including 3 nanometer chips and the emerging 2 nanometer generation.

TSMC has reported profit growth above 50% and expects revenue to grow by more than 30% this year. That is a remarkable expansion rate for a company already at the heart of the global semiconductor industry.

But the impact goes well beyond a single company. Taiwan’s wider economy is becoming more deeply tied to AI infrastructure spending, high-performance computing hardware, and the broader digital supply chain.

Growth numbers that stand out even among developed economies

Taiwan’s government sharply upgraded its 2026 GDP growth forecast to 7.71%, more than double earlier estimates. The main reason cited was stronger-than-expected spending on AI-related infrastructure.

For a developed economy, that is an exceptional growth rate. Export projections have also been revised significantly higher, with shipments expected to increase by more than 22%.

AI-related exports surged nearly 70% at the start of the year, the fastest pace in more than a decade. That pace reflects just how central Taiwan has become to the hardware layer of the AI economy.

As a result, Taiwan’s GDP is expected to surpass $1 trillion for the first time. This is more than a symbolic threshold. It signals that the AI cycle is not just boosting quarterly trade figures. It is changing the scale of the economy itself.

Financial markets are reflecting the shift

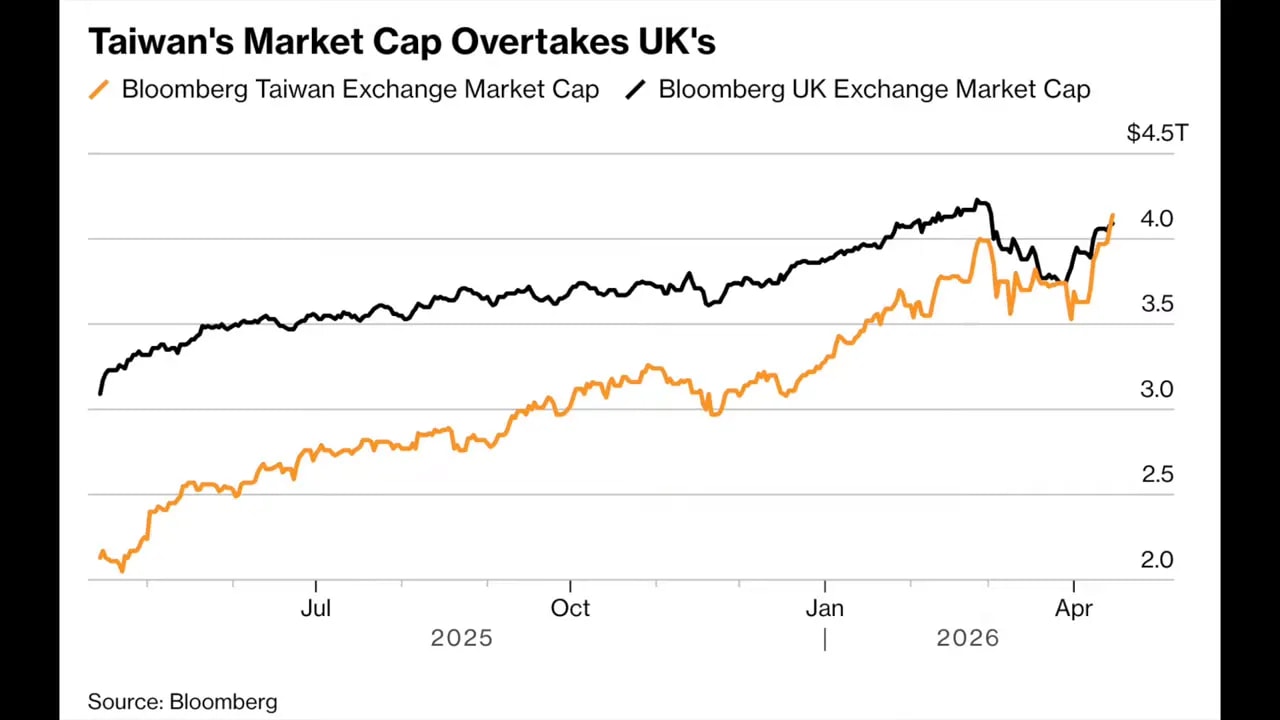

Taiwan’s stock market capitalization has risen to roughly $4.14 trillion, overtaking the United Kingdom to become the world’s seventh largest. The Taiex index has reached record highs, extending a rally led by technology shares.

Foreign investors, who had pulled money out earlier due to geopolitical concerns, have returned in force. Billions of dollars have flowed back into Taiwanese equities as the market increasingly becomes a direct expression of global AI optimism.

Capital spending is reinforcing leadership

TSMC alone plans to spend up to $56 billion in capital expenditure this year. Across Asia’s semiconductor industry, the broader investment push could exceed $130 billion.

That spending does more than add fabrication capacity. It reinforces Taiwan’s ecosystem of suppliers, equipment firms, packaging specialists, and related service providers. In other words, AI demand is strengthening an entire industrial cluster, not just one corporate balance sheet.

Why Taiwan’s geopolitical importance is rising

Taiwan’s role in AI supply chains gives it heightened strategic significance. As competition intensifies over access to advanced technologies, control over the most sophisticated semiconductor production has become a core issue in economic security.

A newly finalized trade agreement with the United States, which reduces tariffs and improves market access, further strengthens Taiwan’s external position. It encourages more investment and deepens ties with Western technology ecosystems.

This does not eliminate geopolitical risk. But it does increase Taiwan’s importance to major economies that depend on advanced chips.

The vulnerabilities behind the boom

The AI surge is highly positive for Taiwan, but it also creates concentrations of risk.

Key vulnerabilities include:

Dependence on continued AI spending. If major technology firms cut capital expenditure, Taiwan would feel the effect quickly.

Infrastructure bottlenecks. Power generation, cooling systems for data centers, and semiconductor capacity can all become constraints.

Rising input costs. Energy disruptions and higher prices for gases and chemicals used in chipmaking could pressure margins.

Uneven domestic benefits. Corporate earnings and exports are surging faster than private consumption, raising questions about income distribution and long-term balance.

Even so, these are problems associated with rapid expansion rather than stagnation. In a world where many developed economies struggle to achieve even modest annual growth, Taiwan’s position is unusually strong.

What these three stories say about the regional economy

Taken together, these developments reveal a stark contrast.

China is trying to stabilize the fallout from a property downturn that has destroyed vast amounts of household wealth. It is also investing heavily in new infrastructure to support the industries it hopes will define the next stage of competition. But that strategy is happening under heavy debt and with growing questions about efficiency.

Taiwan, meanwhile, is benefiting from a global technology wave that is rewarding specialization, industrial depth, and leadership in advanced chips.

This does not mean China is irrelevant to the future of Asian growth. Far from it. But it does show that the drivers of regional economic momentum are changing. Property and construction are no longer the easy engines they once were. Power systems, semiconductors, AI infrastructure, and industrial competitiveness are becoming more central.

That is why China update news now demands attention not only to macro growth figures, but also to the structure beneath them: where wealth is being lost, where capital is being deployed, and which sectors are actually shaping the next economic cycle.

FAQ

Why is China’s housing crisis so important for the broader economy?

Because property has represented an unusually large share of household wealth, local government revenue, and credit creation. Falling home prices weaken consumer confidence, reduce spending, strain banks and developers, and intensify deflationary pressure across the economy.

Is China’s housing market recovering?

Not in a broad national sense. Recent data suggests that price declines are slowing, especially in some major cities, but the market is still contracting overall. Conditions vary sharply by region, and many weaker cities may face years of continued stagnation.

Why is China building so much electricity capacity?

Beijing wants energy security, lower reliance on imports, and abundant power for industries such as AI, robotics, and advanced manufacturing. The strategy also reflects lessons from earlier power shortages that exposed weaknesses in the grid.

What is the main risk in China’s energy expansion?

The biggest risk is that capacity grows faster than economically productive demand. That can create overcapacity, underused assets, weak returns on investment, and rising debt burdens, especially for local governments and state-owned enterprises.

Why is Taiwan benefiting so much from the AI boom?

Taiwan sits at the center of the global advanced semiconductor supply chain. TSMC produces the cutting-edge chips used in AI systems, and strong demand for those chips is boosting exports, profits, investment, and financial markets across Taiwan’s economy.

What could slow Taiwan’s AI-driven growth?

A slowdown in global AI investment, infrastructure bottlenecks, rising materials costs, or tighter semiconductor capacity could all moderate growth. Taiwan’s economy is benefiting greatly from AI, but that also means it is more exposed to changes in the AI spending cycle.