China Update News is increasingly defined by one central theme: surface-level stability is masking deeper strategic and economic strain. Recent developments across geopolitics, the economy, and technology all point in the same direction. China is trying to preserve flexibility abroad, project resilience at home, and accelerate its technological rise, but each of those goals is meeting serious constraints.

The latest developments span three major areas. First, fresh uncertainty has emerged over China’s possible role in the Iran conflict after the United States suggested it had intercepted a suspicious ship linked to Beijing. Second, despite some recent upbeat economic headlines, key indicators suggest China’s recovery remains fragile and uneven. Third, China’s artificial intelligence sector is running into a hard limit: not enough advanced chips, just as Washington moves to tighten semiconductor controls even further.

Table of Contents

- News Section 1: New US-China Friction Over the Iran Conflict

- News Section 2: China’s Economy Is Not Clearly Recovering

- News Section 3: China’s AI Boom Is Hitting a Chip Wall

- News Section 4: The MATCH Act Signals More US Semiconductor Pressure

- What These Stories Have in Common

- FAQ

News Section 1: New US-China Friction Over the Iran Conflict

A new flashpoint has emerged in US-China relations after President Donald Trump suggested that Washington had intercepted a ship carrying suspicious cargo potentially tied to China and destined for Iran. The comments were vague, but the implication was serious.

Speaking in an interview, Trump said the United States had “caught a ship” carrying items that were “not very nice,” then added, “A gift from China, perhaps. I don’t know.” He also remarked that he believed he had an understanding with President Xi Jinping. Although he stopped short of directly accusing Beijing of supplying weapons to Iran, the political message was clear: Washington is signaling that Chinese support for Iran, if proven, could trigger major consequences.

This matters because direct Chinese military aid to Iran during an open conflict involving the United States would cross a major red line. It would not be treated as a minor export-control issue. It would be seen as a challenge to the broader relationship.

At the moment, the details remain unclear. There is still no public confirmation of exactly what was on the vessel. That uncertainty is important. In cases like this, the distinction between weapons, dual-use components, industrial materials, and civilian cargo can determine whether a diplomatic crisis escalates or fades.

Analysts immediately focused on what would happen if the shipment did turn out to include military-relevant goods. One obvious question is whether the United States would follow through on threats to impose steep tariffs or other penalties on countries found to be supporting Iran militarily. Another is whether such a finding would disrupt expected high-level diplomacy between Washington and Beijing.

China moved quickly to reject the implication. A Foreign Ministry spokesperson said the ship seized by the US was a foreign container vessel and rejected what Beijing called false association and speculation. China’s embassy in Washington added that China handles military exports “prudently and responsibly” and strictly controls dual-use goods.

Why China’s position in the Middle East is so sensitive

China’s broader posture toward the Middle East helps explain both the ambiguity and the caution. Beijing has strong economic ties with Iran, especially through energy. China buys roughly 90 percent of Iran’s oil exports, giving Tehran a vital source of revenue. But that does not automatically translate into a full strategic alliance.

In fact, China’s regional strategy has long been based on balance rather than alignment. Beijing has cultivated ties not only with Iran, but also with Saudi Arabia and the United Arab Emirates. Its 2023 role in facilitating a diplomatic thaw between Tehran and Riyadh reinforced the image China wants to project: a commercially engaged power that prefers stability and mediation over military entanglement.

That balancing act is becoming harder. Gulf states have reportedly become more vocal in urging China to pressure Tehran. Meanwhile, any suggestion that Beijing may be helping Iran with intelligence or dual-use items increases suspicion in Washington and in the region.

Energy security is also central. China depends on the Middle East for around 40 percent of its oil imports. That makes free passage through the Strait of Hormuz and broader regional stability a core national interest. Xi Jinping has called for de-escalation and for the restoration of normal shipping conditions, a position that reflects both strategic caution and economic necessity.

There is another reason Beijing is likely to be careful. Trade with Iran is highly asymmetric. Iran accounts for less than 1 percent of China’s total commerce, and major Chinese firms remain cautious because of secondary US sanctions. Big headline commitments have often not translated into equally large flows of actual investment.

The result is a relationship that is important, but bounded. China gains from buying discounted oil and maintaining diplomatic access, yet it also has strong incentives to avoid being drawn into a direct confrontation with the United States over Iran.

News Section 2: China’s Economy Is Not Clearly Recovering

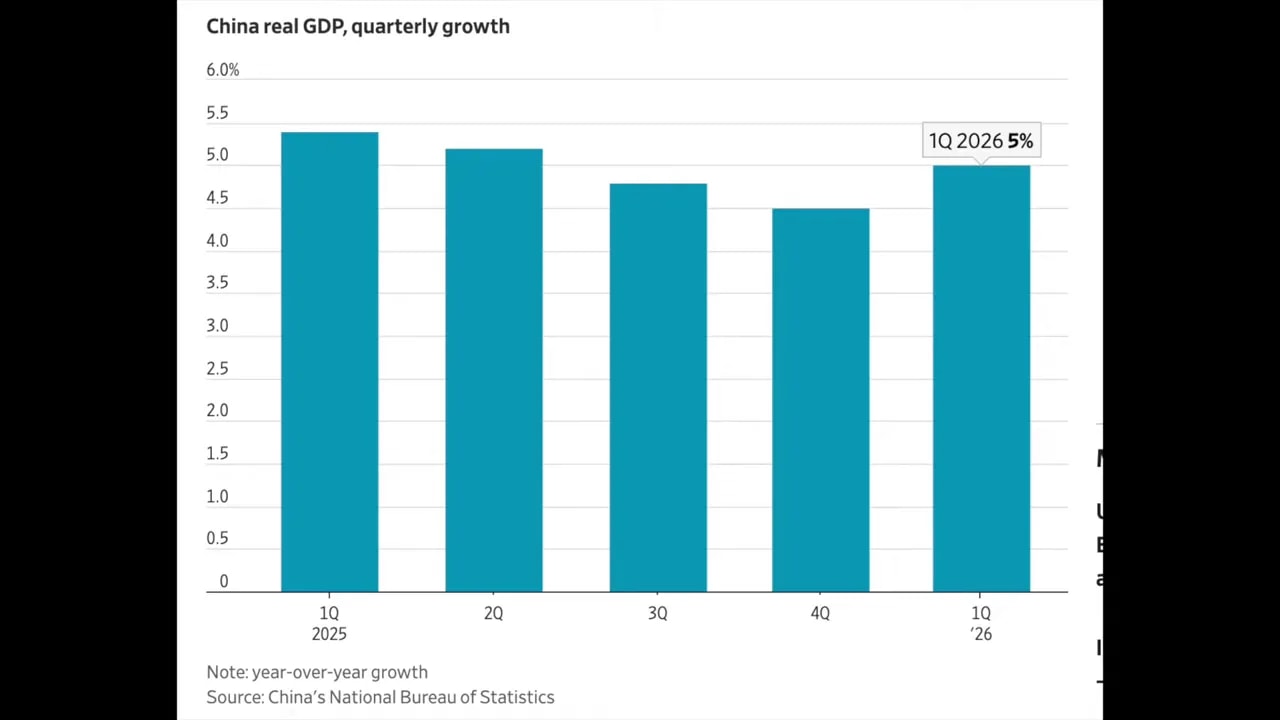

A growing number of headlines have suggested that China’s economy may finally be stabilizing. There are some reasons for that view. Recent GDP growth came in stronger than many expected. Some property indicators have shown early signs of improvement. Equity markets have rebounded from lows. Producer prices have also moved out of deflation.

But those datapoints do not, by themselves, prove that China has turned a corner. The more important question is what is driving the improvement. On that point, the picture is much less reassuring.

The strongest recent GDP figure, about 5 percent in the first quarter, was driven largely by state-led investment and subsidized manufacturing for export. That is not the same thing as a broad-based recovery led by household demand and private business confidence. In fact, consumption and private investment remain weak.

The same pattern appears in prices. China did emerge from producer-price deflation recently, but the change was tied to rising input costs linked to the Middle East conflict rather than stronger domestic demand. In other words, firms were paying more for inputs, not selling much more to consumers. If companies cannot pass those costs on, profit pressure rises instead of easing.

Market data also requires caution. The CSI 300 has gained substantially from its depressed levels, but it remains well below its 2021 high. That makes the rebound real, but limited. A market can recover from an oversold state without signaling a durable macroeconomic turnaround.

Employment data reveals persistent weakness

The labor market is another reason to be skeptical of overly optimistic narratives. Official data showed that China’s youth unemployment rate rose to 16.9 percent in March, up from 16.1 percent in February. That increase broke a normal seasonal pattern in which employment typically improves after the Lunar New Year.

The timing is especially concerning because a record 12.7 million graduates are expected to enter the job market this year. That adds pressure to an already competitive environment.

The broader urban unemployment rate rose to 5.4 percent, the highest in a year, and also increased across 31 major cities. The weakness appears particularly significant for those aged 25 to 29, a cohort that traditionally includes many early-career workers making the transition from education into stable employment.

This group may also face additional pressure from automation and AI-related disruption in white-collar and entry-level roles. That does not mean AI is already the main cause of the problem, but it highlights another layer of labor-market vulnerability at a time when consumer confidence is already fragile.

The deeper debate: recovery or prolonged adjustment?

The real debate among economists is not whether China can produce a few better monthly numbers. It is whether the country is experiencing the start of a durable recovery or moving through a long structural adjustment.

One influential view, associated with economist Kenneth Rogoff and co-authors in a National Bureau of Economic Research working paper, is that China is still in the middle of a multi-year correction with parallels to Japan’s bubble and post-bubble period. Their argument is that China’s adjustment is taking place in a tougher macroeconomic and demographic environment than Japan faced.

At the same time, they note an important difference: China’s state-dominated financial system and proactive policy intervention have so far prevented a full financial-sector breakdown. That is not the same as solving the underlying imbalances, but it does reduce the odds of a sudden collapse.

A more optimistic camp argues that the worst of the property slump may already be over and that China’s intensely competitive business environment can still generate stronger, more productive firms. This view places heavy emphasis on innovation, especially under pressure from strategic competition with the United States.

Even so, there is no clear consensus. Some analysts remain far more cautious on property, arguing that the downturn may continue for at least another two years before reaching a bottom. Given the role of housing in household wealth, local government finance, and credit creation, that difference in outlook is hugely consequential.

What the caveats really mean

The most important takeaway is that headline indicators are not enough. China still faces several structural challenges:

A weakened property sector that continues to drag on confidence and local finances

High local government debt that limits policy flexibility

Demographic decline that weighs on long-term growth

Weak consumer confidence that limits demand-led recovery

Soft private investment despite strong state support in selected sectors

That combination does not rule out improvement. It does mean, however, that declaring victory based on a handful of positive indicators is premature. The economy looks mixed at best, and some of the apparent good news becomes less impressive once the underlying drivers are examined.

News Section 3: China’s AI Boom Is Hitting a Chip Wall

The next major story concerns China’s rapidly expanding AI industry. Demand is surging, but compute supply is not keeping up. That mismatch is now becoming a genuine bottleneck.

Chinese financial media has reported that many leading AI companies are facing service disruptions because of limited access to computing power. Firms such as Minimax, Moonshot AI, and Zhipu AI have reportedly experienced throttled APIs, temporary service suspensions, and unstable performance. DeepSeek suffered an outage lasting nearly 12 hours, underlining just how strained the infrastructure has become.

The problem is no longer theoretical. Chinese AI firms are already rationing access, raising prices, and reconsidering growth strategies.

How the shortage is showing up

The strain is visible across the sector:

API access has been restricted or paused during periods of high demand

Cloud providers have imposed quotas and limited high-frequency usage

Some AI services and subscription tiers have sold out

Prices for usage and subscriptions have increased

Developers have become more cautious about embedding AI into mission-critical systems

Inside major firms, computing resources are being prioritized. Reports indicate that teams at Alibaba scaled back non-essential operations during peak usage periods, while ByteDance temporarily disabled some features during the Spring Festival to reduce the risk of system failures.

One especially demanding category is AI coding tools. These applications consume far more compute than standard chatbot interactions. In some cases, AI agents performing multi-step tasks may require tens or even hundreds of times more tokens per task than simple conversational use. As adoption spreads, demand for advanced chips and server capacity rises very quickly.

Why advanced chips remain the key constraint

At the hardware level, China still faces severe limits in obtaining the most advanced GPUs and semiconductor tools. Those restrictions are the result of both export controls and physical supply bottlenecks in global chip manufacturing.

Advanced production remains heavily dependent on Taiwan Semiconductor Manufacturing Company. Capacity expansion takes years, and demand is intense across the global industry. Even without geopolitics, supply would be tight. With geopolitics, it becomes far tighter.

This is why the chip shortage carries broader significance. It suggests that US restrictions, despite loopholes and leakage, may still be imposing meaningful costs on China’s AI ecosystem. Innovation alone cannot overcome an infrastructure deficit if the hardware is not available in sufficient quantity or quality.

The implication is not that China’s AI ambitions are collapsing. It is that the pace and shape of expansion may be constrained by compute access as much as by algorithmic progress.

News Section 4: The MATCH Act Signals More US Semiconductor Pressure

The final major development reinforces that point. In Washington, the MATCH Act advanced out of the House Foreign Affairs Committee with strong bipartisan support. The bill is aimed at tightening export restrictions on semiconductor tools and closing loopholes that have allowed some support for advanced Chinese chipmaking to continue.

China Update News in the technology space increasingly revolves around this reality: the contest is not just about who designs better AI models. It is also about who controls the hardware, the supply chains, and the servicing ecosystem behind those models.

What the MATCH Act would do

The legislation would significantly tighten restrictions on the sale and servicing of critical semiconductor manufacturing equipment to advanced fabrication facilities in China. It would still allow certain limited activities by US- or allied-controlled operations in China, but the overall direction is unmistakable: less access, fewer loopholes, and shorter operational life for high-end production capacity.

The targeted tools include deep ultraviolet lithography systems and advanced etching technologies, both essential for making sophisticated chips. If enacted, the bill would expand constraints on major Chinese companies such as:

SMIC

Huawei

Hua Hong

ChangXin Memory Technologies

Yangtze Memory Technologies

One especially consequential feature is that the bill would restrict not only new equipment sales, but also maintenance and technical support for existing equipment. That matters because a machine’s usefulness depends heavily on servicing, parts, and software updates. Without those, installed tools gradually become less effective and more difficult to operate at high performance.

Why this matters beyond one bill

The legislation builds on years of coordinated US efforts with the Netherlands and Japan to limit China’s access to the most advanced chipmaking systems. Since 2018, those efforts have focused especially on keeping extreme ultraviolet lithography machines out of China. But important gaps remained, especially around older systems and installed equipment servicing.

The MATCH Act is designed to narrow those gaps. It has not become law yet, and political questions remain, including whether the White House would fully support it. But the larger trend is already clear. In Washington, there is a growing bipartisan consensus that semiconductor restrictions are a central tool of competition with China.

That means the AI race is becoming inseparable from export control policy. Compute capacity, manufacturing tools, and maintenance support are no longer background issues. They are frontline strategic assets.

What These Stories Have in Common

These developments may appear separate, but they are linked by a common pattern.

In foreign policy, China is trying to maintain strategic ambiguity in the Middle East while preserving ties on all sides. In the economy, it is trying to stabilize growth without having solved deep structural weaknesses. In technology, it is trying to scale AI leadership while facing tightening hardware constraints from abroad.

In each case, the same basic tension appears: Beijing wants room to maneuver, but that room is narrowing.

The Iran issue shows how quickly a murky logistics question can become a high-stakes diplomatic confrontation. The economic data shows why optimistic headlines can be misleading when growth is still heavily dependent on state support. And the chip shortage, combined with the MATCH Act, shows that strategic competition is increasingly being decided by control over bottlenecks rather than by broad declarations of national ambition.

China Update News therefore points less to a clean recovery and more to a complicated period of adjustment. China remains capable, influential, and economically significant. But the constraints are becoming harder to ignore.

FAQ

Why is the intercepted ship linked to Iran such a significant issue for China?

Because any evidence that China directly supplied military-related goods to Iran during a conflict involving the United States would cross a major political red line. It could damage planned diplomacy, trigger sanctions or tariffs, and intensify already strained US-China relations.

Is China fully aligned with Iran in the Middle East?

No. China has important economic ties with Iran, especially through oil purchases, but it also maintains strong relations with Saudi Arabia, the UAE, and other regional powers. Beijing’s approach has generally been to balance relationships rather than formally align with one side.

Why do some analysts say China’s economy is not truly recovering?

Because several recent positive indicators have weak foundations. GDP growth has been driven largely by state-led investment and exports, not stronger consumption. Producer prices improved because of higher input costs, not stronger demand. Youth unemployment and broader labor-market weakness also remain serious concerns.

What is the biggest economic risk facing China right now?

There is no single risk, but the property downturn remains central because it affects household wealth, local government finances, investment, and confidence. High debt, demographic decline, and weak consumer demand add to the challenge.

Why is China’s AI industry facing service disruptions?

The core issue is insufficient computing power. Demand for AI services is rising quickly, especially for compute-intensive applications like coding tools and AI agents. But access to advanced chips is limited, leading firms to ration services, impose quotas, and raise prices.

What is the MATCH Act and why does it matter?

The MATCH Act is proposed US legislation that would tighten restrictions on semiconductor equipment exports and servicing for advanced Chinese chip facilities. It matters because maintenance and technical support are essential to keeping chipmaking equipment operational. Restricting both sales and servicing could significantly increase pressure on China’s semiconductor industry.

What is the broader takeaway from these developments?

The broader takeaway is that China is facing growing constraints across multiple fronts at once. Geopolitical ambiguity is harder to maintain, economic stabilization remains incomplete, and technological progress is increasingly shaped by access to scarce hardware and external controls.