China Update News is increasingly shaped by maritime risk, supply chain stress, and financial strain that are no longer confined to distant headlines. In recent developments, China has signaled dissatisfaction with U.S. naval actions tied to Iran, while economists and market watchers point to rising costs in key industrial inputs. At the same time, official debt and financing metrics suggest the economy is still fighting to meet growth expectations. Finally, Taiwan is reportedly stepping up drills for potential maritime disruption, even as financial markets appear to look through geopolitical risk.

Table of Contents

- 1) China signals mounting distress over U.S. blockade targeting vessels linked to Iran

- 2) Energy and commodities stress ripples into China’s industrial system

- 3) Internal debate: some Chinese analysts dispute the idea that the Iran war benefits China

- 4) Inflation picture: producer prices turn positive while consumer demand remains weak

- 5) Official debt and financing data suggest chasing growth with more leverage

- 6) Taiwan steps up blockade readiness as maritime choke points become a planning priority

- 7) Markets remain resilient even as geopolitical risk rises

- FAQ

- Bottom line

1) China signals mounting distress over U.S. blockade targeting vessels linked to Iran

Beijing has publicly indicated growing displeasure regarding U.S. naval actions described as disrupting shipping associated with Iran and transiting through the Strait of Hormuz. China’s concern is not only diplomatic. It is also economic and logistical, because the Strait is a major global choke point for energy and commodity flows.

In the official framing, maintaining secure and unimpeded passage through the Strait aligns with the “common interests of the international community,” and resolving the broader crisis through an urgent ceasefire has been urged. China, however, stopped short of directly challenging U.S. actions, underscoring a key constraint: China’s ability to counterbalance U.S. naval power is limited.

The practical risk for China is straightforward. Prolonged interference with shipping in and around Hormuz would likely tighten supply, raise costs, and deepen pressure on an economy already dealing with slower growth and uneven demand conditions.

Why the Strait of Hormuz matters for China’s economy

The Strait of Hormuz is repeatedly highlighted as critical because it supports a large share of shipments tied to global energy flows. The transcript notes that a significant portion of shipments is bound for China. That makes Hormuz-related disruptions especially relevant to China’s import-dependent industrial system.

Even when direct military confrontation is absent, maritime risk can translate into higher freight and insurance costs, delayed cargoes, and uncertain delivery schedules. Those disruptions can cascade quickly into industrial input markets.

Diplomatic pressure increases: UAE outreach to Beijing

The situation is not evolving purely through military channels. A visit by the UAE Crown Prince to Beijing is described as likely related to encouraging China to push for Iran to stop targeting Gulf states. China’s foreign minister, Wang Yi, reaffirmed support for Gulf states’ security concerns, without providing operational details.

For analysts cited in the transcript, Beijing is displeased by the blockade of ships leaving Iranian ports and transiting Hormuz, but unclear about what it can do to stop the U.S. action. The risk, they argue, is that a prolonged blockade would add further stress to China’s economy, including for shipments that are distant from China.

2) Energy and commodities stress ripples into China’s industrial system

As the conflict dynamics tied to Iran progress, the economic impact for China is described as becoming more visible. Early in the disruption, some analysts believed China was relatively well prepared because of prior efforts to insulate supply chains from external shocks. However, six weeks into the crisis, stress is increasingly apparent across pricing and availability of industrial inputs.

Key symptoms: rising energy costs and disrupted supply flows

The transcript describes several measurable and market-based signals:

- Higher energy and input costs that push up prices for industrial commodities.

- More pressure in petrochemicals and advanced materials, where feedstock supply is especially sensitive to shipping disruptions.

- Shortages and steep price jumps for critical industrial glass and helium supplies, which are described as important for semiconductors and medical technology.

- Price spikes exceeding 100% for high-grade helium supplies in recent weeks (as referenced in the transcript).

These are not isolated sectors. When energy-intensive and materials-intensive industries face cost increases, knock-on effects typically reach logistics, steel, aviation, and export-oriented manufacturing.

Middle East dependence amplifies the impact

A central factor mentioned is China’s reliance on the Middle East for energy and chemical feedstocks. Before the conflict, the Middle East supplied about one-third of China’s oil and a quarter of its natural gas, along with key inputs for chemical production.

With shipping disruption concentrated around Hormuz, the uncertainty about when normal supply flows resume becomes a persistent economic variable rather than a temporary shock.

Cascading effects across sectors

According to the transcript, the disruption cascades into multiple layers of the economy:

- Energy-intensive sectors including logistics, steel, and aviation facing cost increases of up to 25%.

- Margin squeezing that places smaller firms under pressure.

- Export-oriented manufacturers adjusting by scaling back orders or raising prices to respond to raw material cost surges.

In response, Beijing is described as acting cautiously. It has imposed export restrictions on certain fuels and fertilizers to protect domestic supply and is considering broader tools such as releasing strategic reserves.

3) Internal debate: some Chinese analysts dispute the idea that the Iran war benefits China

Not all analysis in China is optimistic. The transcript notes that a set of Chinese articles portrayed the Iran war as a blow to the U.S. and potentially an opportunity for China. However, additional commentary from Chinese analysts warns that the risks to China may be systemic and sustained.

Commodity volatility as a systemic risk

Peng Xiaozong, formerly a senior analyst at the National Development and Reform Commission and later vice president of a state-affiliated think tank, is cited as arguing that commodity price volatility triggered by the U.S.-Iran escalation could create a systemic impact on China’s economy, potentially leading to repeated disruptions.

A separate warning from Cameron Johnson, a senior partner at a supply chain consultancy, goes further. The transcript states that supply disruptions could become worse than during the COVID-19 pandemic, with some prices in China doubling for certain inputs. The example provided includes a market impact spanning materials used for consumer goods, such as plastic bottles and clothing, as well as carbon fibers that depend on feedstocks linked to the Middle East.

The transcript also mentions that carbon fiber prices could rise around 20%, with usage across auto and consumer goods industries.

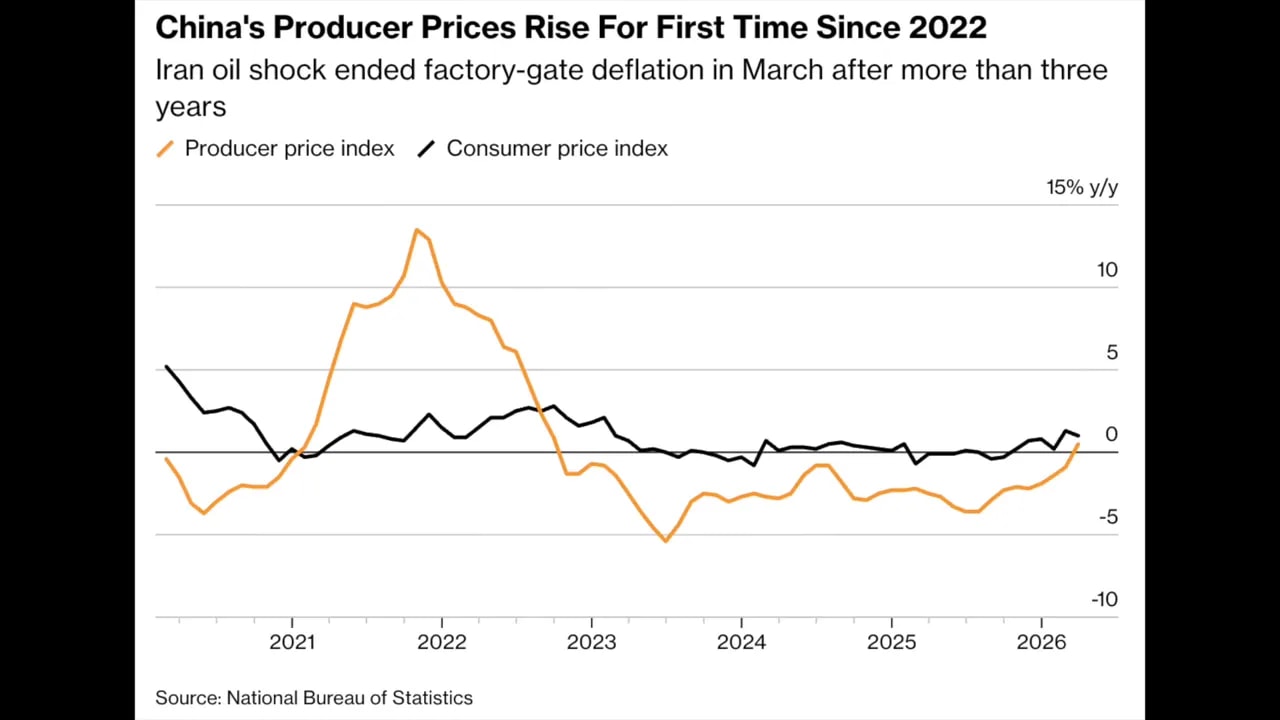

4) Inflation picture: producer prices turn positive while consumer demand remains weak

One of the most important macroeconomic questions is whether higher costs translate into consumer inflation and broader demand recovery. The transcript describes a divergence: producer price inflation returns, but consumer price inflation remains subdued.

Factory gate inflation (PPI) rises year-on-year

Data from China’s National Bureau of Statistics is described as showing that producer prices (PPI) rose 0.5% year-on-year in March. That outcome ends a 41-month streak of declines that had ended only once the Iran war-driven increase in global energy costs pushed input costs higher.

On a monthly basis, PPI climbed 1%, the fastest pace in four years, reflecting sharper rises in oil and industrial commodities.

But consumer inflation stays low

In contrast, the consumer price index (CPI) is described as slowing to 1%, with core inflation easing further. The interpretation in the transcript is that domestic demand remains subdued.

This divergence suggests that manufacturers absorb much of the cost pressure rather than passing it through fully to consumers. With raw material prices rising faster than selling prices, profit margins remain under strain.

Policy implication: inflation rebound is cost-driven, not demand-driven

Even though PPI has turned positive, the transcript emphasizes that this is driven largely by external cost shocks. The argument presented is that the economy may be exiting deflation in a fragile way, not experiencing sustainable resilience.

In practical terms, policymakers may face a challenging tradeoff. If producers cannot pass costs to consumers, growth could remain weak even while certain inflation measures rise. If the cost shock persists, margins and employment can come under pressure despite nominal inflation improvement.

5) Official debt and financing data suggest chasing growth with more leverage

Beyond supply costs and inflation dynamics, financing conditions matter. The transcript highlights a discussion of official debt numbers, referencing analysis by Michael Pettis, a professor of finance at Peking University.

New financing declines, but the net increase in aggregate financing still looks heavy

According to the transcript, a report citing People’s Bank of China data states:

- Aggregate new financing in Q1 2026 totals 14.83 trillion yuan.

- This is 2.3% less than Q1 2025, with more than 100% of the decline concentrated in March.

The analysis also frames the amount as large relative to economic output. It describes the financing level as roughly 42% of one quarter’s GDP, using assumptions about interest on outstanding debt.

The transcript’s calculation indicates that net growth in aggregate financing in March is 5.23 trillion yuan, about 11.2% lower than the prior March. That pattern is associated with expectations that first quarter GDP growth may come in below 4.8%.

Core takeaway: more debt created to chase less growth

In summary, the interpretation presented is that China is behind its targets and that more debt is being created to pursue growth that is increasingly difficult to deliver. This does not automatically mean debt is unsustainable in every scenario, but it does highlight an important structural tension: financing momentum may not be translating into robust nominal growth.

6) Taiwan steps up blockade readiness as maritime choke points become a planning priority

Geopolitical risk is also moving into concrete readiness planning. The transcript states that Taiwan is preparing for potential maritime blockade scenarios through new drills focused on protecting critical energy and supply routes.

Drills focus on escorting fuel and maintaining corridors

Reported exercises are described as testing:

- Escort operations for fuel shipments.

- Maintaining three maritime corridors linking Taiwan to the Philippines, Japan, and the United States.

Emergency logistics and aid vessel docking

Later drills planned within the year are described as focusing on:

- Docking international aid vessels.

- Handling emergency logistics.

- Distributing supplies across Taiwan in a crisis scenario.

Why this matters for regional trade networks

The transcript includes the warning from Taiwan’s deputy interior minister that any blockade would disrupt regional energy flows beyond Taiwan itself. This is a key point for the wider region: maritime choke point disruption typically affects supply chains and energy pricing in multiple countries, not just the frontline economy.

The drills come amid rising military pressure from Beijing, which continues to assert sovereignty over Taiwan. Although China is described as not explicitly threatening a blockade, large-scale exercises simulating encirclement are said to have sharpened Taipei’s focus on readiness.

7) Markets remain resilient even as geopolitical risk rises

One of the most interesting dynamics in the transcript is the divergence between rising risk and market behavior. Despite the heightened maritime and geopolitical stress, financial markets are described as remaining notably resilient.

Equities: Taiwan benchmark hits record highs

The transcript notes that Taiwan’s benchmark stock index has surged to record highs, erasing earlier losses linked to the Iran war.

Why investors are focusing on the AI supply chain

Investors appear to be placing weight on Taiwan’s role in advanced chip production. Specifically, attention is on TSMC (Taiwan Semiconductor Manufacturing Company), described as central to advanced semiconductor manufacturing used by major AI developers, including Nvidia.

The logic presented is that strong revenue growth at TSMC, driven by sustained demand for high-performance chips, has reinforced confidence that geopolitical shocks have not derailed the broader technology cycle.

But the equilibrium is fragile

Even with bullish equity pricing, the transcript argues that structural dependence on secure surrounding seas remains. Taiwan’s “dominance” in critical supply chains offers a structural advantage, but it does not eliminate the underlying exposure to maritime routes and regional security.

In other words, markets may be pricing continued growth and stability, while operational risk rises in parallel.

FAQ

What is the Strait of Hormuz risk described in this China Update News?

It refers to the risk that disruptions or a prolonged U.S. naval blockade affecting ships linked to Iran could interfere with secure and unimpeded passage through the Strait. Because it is a major global energy choke point with shipments bound for China, any interference can raise costs and tighten supply for China’s economy.

How is inflation changing in China according to the producer and consumer data?

Producer inflation (PPI) rose 0.5% year-on-year in March, ending a long decline streak, largely due to external cost shocks like higher energy prices. Consumer inflation (CPI) remains weak at 1%, suggesting domestic demand is subdued and costs are not fully passing through to consumers.

What does the debt commentary suggest about China’s growth strategy?

The commentary highlights that aggregate new financing in Q1 2026 is still very large relative to GDP, while growth appears behind expectations. The interpretation is that more debt may be needed to pursue less growth, increasing strain on the balance between financing and real economic performance.

Why is Taiwan increasing blockade-related drills?

The transcript states that Taiwan is preparing for potential maritime blockade scenarios by running exercises focused on protecting energy and supply routes. These drills include testing escort operations for fuel shipments and maintaining key maritime corridors, as well as emergency logistics for aid and supplies.

Bottom line

These developments collectively reinforce a single theme: China’s exposure to global maritime chokepoints and energy supply flows is showing up in both economic indicators and policy concern. With producer inflation turning positive from cost shocks, debt and financing pressures still evident in official metrics, and Taiwan tightening blockade readiness, China Update News increasingly reads like an integrated risk assessment rather than separate stories.

For businesses and investors, the key lesson is not only that geopolitical risk exists, but that it travels through practical channels: freight and insurance costs, commodity pricing, industrial input availability, profit margins, and ultimately confidence in growth.