China Update News for this week focuses on a familiar pattern: early signs of improvement in parts of the economy, alongside stress tests that could quickly overwhelm the gains. Industrial profits appear to be rebounding, but the rebound arrives with a major caveat. China is also leaning heavily on infrastructure as growth softens. At the same time, Beijing is pushing science spending toward a new scale, while tightening regulation in consumer markets after years of subsidy-fueled competition.

Table of Contents

- 1) Industrial profits surge in early 2026, but the base effect is doing a lot of work

- 2) China opens a “Goddess Escalator” in Chongqing, another reminder that infrastructure still carries policy weight

- 3) China is on track to overtake the United States in public science funding

- 4) Beijing cracks down on the food delivery price war, aiming to end “subsidy-driven competition”

- What ties these stories together?

- FAQ

- Summary

1) Industrial profits surge in early 2026, but the base effect is doing a lot of work

On the surface, the start of 2026 looks encouraging for China’s industrial sector. In the first two months of the year, industrial profits rose 15.2% year on year. That is described as the strongest opening since 2018, excluding distortions during the pandemic period.

The National Bureau of Statistics data also points to stabilization in the manufacturing base after weak performance. The improvement is linked to better demand conditions and easing deflationary pressures, both of which help firms convert sales into profits rather than fighting just to keep revenue alive.

The key context: 2025 was weak, so 2026 is rising from a low platform

Still, the turnaround is best understood as coming off a fragile period. In 2025, industrial profits grew only 0.6% after three consecutive years of decline. When analysts describe early 2026 strength as “more durable,” they are not denying the improvement, but they are essentially saying the recovery may be more grounded than it looked in the past.

One supporting factor is policy aimed at curbing aggressive price competition. The logic is straightforward: if firms stop cutting prices to win market share at any cost, pricing power can gradually return, margins can stabilize, and profit metrics will improve even before demand becomes dramatically stronger.

Winners are concentrated: high-tech manufacturing is driving the better numbers

Where the news becomes more interesting is in the composition of the rebound. Much of the profit growth is coming from high-technology manufacturing. The electronics sector stands out: profits there jumped more than 200% year on year, supported by the global boom in artificial intelligence.

That AI-linked demand matters because it pulls on multiple parts of China’s supply chain:

- Semiconductor demand and related equipment needs

- Power equipment used to support data infrastructure

- Export revenues for chip-related firms

Even with geopolitical frictions, these supply chain connections appear to be intact enough to keep supporting Chinese exporters. Upstream industries linked to non-ferrous metals also helped. Earlier rallies in commodity prices such as copper and aluminum appear to have benefited mining and smelting operations.

The big threat: an energy shock could squeeze margins fast

Here is the “devil in the detail” part. The profit rebound happens before what the latest analysis describes as a developing energy shock that threatens to smash input costs across industry.

The catalyst is the escalation of the war with Iran, which has pushed global energy prices higher. Crude prices are described as up roughly 90% year to date. For industrial operators, energy is not just a line item. It flows into costs for key inputs, particularly in:

- Chemicals

- Plastics

- Synthetic fibers

The result is a squeeze on downstream margins. And because China is heavily reliant on imported energy, the downside can land especially hard. In other words, even if higher energy prices benefit some upstream producers, the broader effect on an energy-intensive manufacturing model is likely negative.

Margins are already fragile. In 2025, profit margins fell to 5.3%, the lowest level in over a decade. When margins are thin, volatility in input costs can quickly turn a “recovery” into a fresh deterioration.

Bottom line: the industrial rebound in early 2026 is real, but it is not a guarantee of stability. It is partly a comparison to a low base, and it faces a new external stress test from energy markets.

2) China opens a “Goddess Escalator” in Chongqing, another reminder that infrastructure still carries policy weight

China has unveiled what is widely described as the world’s longest outdoor escalator system. The “Goddess Escalator” is located in Wushan County in Chongqing along steep banks of the Yangtze River.

The system stretches nearly one kilometer and takes about 21 minutes to ascend. Completed over more than four years, the project includes more than two dozen escalators and lifts designed to address the region’s rugged terrain. Engineers describe it as unprecedented in scale, reflecting the geographic constraints of southwestern China.

Usage is real, but the policy trade-offs are bigger than the headline

Roughly nine thousand people use the escalator daily, paying a small fee. That journey previously could take up to an hour by road during peak traffic. For many residents, the value is immediate: a demanding commute becomes more accessible.

Tourism has also moved in quickly. The escalator is now a local landmark, and Chongqing is known for drawing visitors who enjoy futuristic-looking infrastructure and dramatic engineering.

Why this matters economically: infrastructure remains a key lever

The deeper point is what this says about China’s economic model. Even as property has weakened and overall growth has moderated, infrastructure investment continues to function as a major policy tool, especially in less developed inland regions.

Analysts note that these projects are among the few levers Beijing can directly control to support domestic demand. That also explains why concerns about debt persist. Infrastructure spending can provide near-term economic momentum, but it can raise the risk of diminishing returns when projects do not generate enough economic activity for the cost.

Chongqing, in particular, is mentioned as a region that has faced accusations of being in a de facto bankruptcy situation. Add to that the environmental and maintenance complexity of operating an outdoor system at scale in mountainous conditions, and the long-term debate becomes unavoidable.

Bottom line: the escalator is a striking engineering solution to terrain. But it also highlights the policy reliance on infrastructure when other growth engines, like property, are no longer reliably supportive.

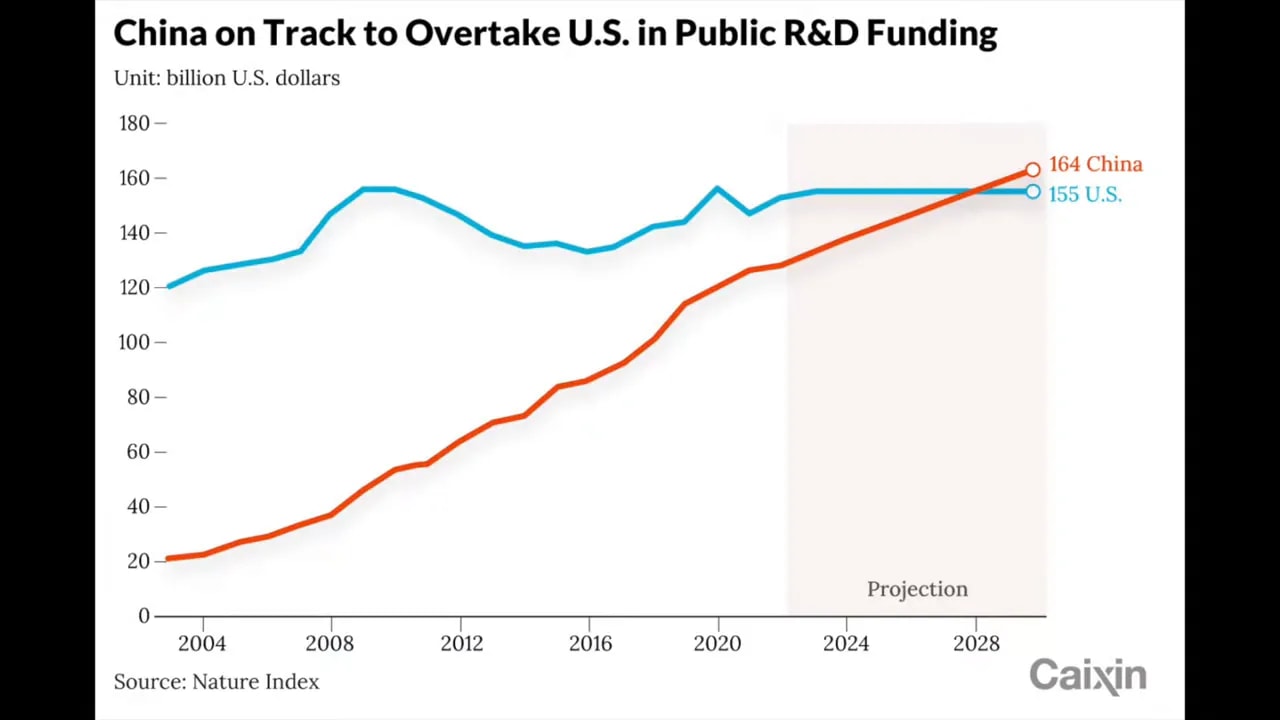

3) China is on track to overtake the United States in public science funding

Another “big picture” signal in this week’s China Update News is scientific research funding. China appears on track to become the world’s largest public funder of scientific research, potentially within the next two to three years.

R&D spending: China’s rise versus the US

A Nature Index analysis, drawing on research from the University of California, San Diego, estimates that Chinese government R&D spending surged by roughly 90% between 2013 and 2023, reaching about $133 billion. Over the same period, US spending rose just 12% to about $155 billion.

It is important that the comparison is specifically about public funding, not private sector research and development. The analysis notes that the US still maintains a healthy lead in private R&D, which is often linked to commercialization strength and tech entrepreneurship.

Could the US lose its public funding dominance by 2028?

If the trend continues, China could surpass US public research spending as early as 2028. Analysts describe this as a potential watershed event because it would end decades of US dominance in public funding since World War II.

Structural shifts: more diverse funding and faster R&D growth targets

Scale is one thing, but structure is another. Chinese research funding is also evolving. Saizen, a Chinese financial media outlet, reports that the latest five-year plan targets annual R&D growth of at least 7%, while increasing contributions from private companies alongside government funding.

This matters because a more mixed funding model can widen the pipeline from basic research to applied innovation. In theory, it can also improve responsiveness to market needs while still supporting long-term national priorities.

The gap remains: basic research is still behind

However, a key concern remains: basic research. In 2023, China spent around $53 billion on basic research, less than half of US levels. The hope is that faster growth in basic research spending could help narrow the gap over the next decade, but it is not something that closes instantly.

There is also a geopolitical layer to all of this. The “geography of science” appears to be shifting. Chinese institutions are gaining ground in high-impact research output and attracting more international talent. At the same time, collaboration with Western partners is declining amid geopolitical tensions.

Bottom line: China’s public science funding is accelerating. If private funding patterns do not keep the US firmly ahead, China could change the global innovation balance in the public sector, even if basic research depth and private sector capacity still matter.

4) Beijing cracks down on the food delivery price war, aiming to end “subsidy-driven competition”

The final and most policy-driven story is China’s intensifying regulatory push to end the food delivery price war. This is the kind of shift that often has ripple effects throughout consumption, inflation dynamics, and employment in low-margin services.

Regulators want to end the subsidy arms race

According to a commentary published by the state-run Economic Daily and amplified by the state administration for market regulation, the era of aggressive subsidy-driven competition in the takeout sector may be coming to an end.

Regulators have already launched on-site investigations into major delivery platforms. That raises the expectation that stricter anti-monopoly enforcement is imminent.

For years, China’s delivery giants, including Meituan, Alibaba, and JD.com, have reportedly engaged in a costly battle for market share, collectively spending up to 100 billion yuan in subsidies.

Consumers benefited in the short term through ultra-cheap meals and discounts. But the macro consequences have become increasingly visible.

Why price wars distort the economy: inflation, deflation, and a business squeeze

The core issue is price distortion. The catering sector accounts for nearly 30% of China’s consumer price index (CPI) basket, making it a critical driver of headline inflation trends.

During the peak of the subsidy war in 2025, restaurant prices fell sharply, dragging down headline CPI, even as underlying demand showed signs of tacit recovery. In other words, artificial price suppression may have masked broader consumption trends and contributed to deflationary pressure.

For businesses, the impact appears severe. Restaurants squeezed by platform fees and forced discounting have seen profits collapse. In some cases, average transaction values are described as reverting to levels seen about a decade ago.

That creates a vicious cycle:

- Lower prices lead to weaker revenues

- Weaker revenues lead to reduced hiring

- Reduced hiring slows income growth

- Slower income growth undermines domestic consumption

The policy logic: shift from growth at any cost to stability

From a macro perspective, regulators now appear to view the price war as a form of “involution,” meaning destructive competition that erodes long-term economic health. Ending it is not only about fair competition. It is also about stabilizing a sector that matters for employment and for the CPI.

Bottom line: Beijing is signaling that competition should shift from burning capital to improving efficiency, technology, and service, aligning platform incentives with the broader economic goal of steadier prices, profits, and jobs.

What ties these stories together?

Across industrial profits, infrastructure build-outs, rising public science funding, and delivery market regulation, a common theme emerges. Policy and economic performance are increasingly being managed through targeted levers rather than broad-based growth optimism.

- Industry is improving, but external costs like energy can quickly reverse gains.

- Infrastructure remains a controllable demand stimulus, but the debt and efficiency questions do not disappear.

- Science funding is scaling fast, potentially changing global public research leadership, but basic research depth remains a gap.

- Market regulation is shifting away from subsidy-driven competition toward stabilizing prices and supporting sustainable employment.

That is the reality of the moment: China Update News this week reads less like a simple recovery story and more like a series of tests. Some areas are pushing forward. Others are being reined in. And in both cases, policy is responding to constraints.

FAQ

How much did China’s industrial profits rise in the first two months of 2026?

Industrial profits rose 15.2% in the first two months of 2026 year on year.

Why is the industrial rebound in 2026 considered less positive than it appears?

Because it is partly a rebound from a very low base after weak 2025 performance, and it arrives as an energy shock threatens to raise input costs and squeeze margins further.

What is the “Goddess Escalator” and where is it located?

It is a very large outdoor escalator and lift system in Wushan County in Chongqing along the Yangtze River banks.

What research funding comparison suggests China could surpass the United States?

Chinese government R&D spending rose about 90% from 2013 to 2023 to around $133 billion, while US public R&D rose about 12% to around $155 billion. If trends continue, China could surpass US public spending by around 2028.

What is Beijing doing regarding the food delivery price war?

Regulators are pushing to end subsidy-driven competition, including launching on-site investigations into major platforms and signaling stricter anti-monopoly enforcement.

Why does the delivery price war matter for inflation and the broader economy?

Catering makes up nearly 30% of China’s CPI basket. Artificial price suppression can distort inflation readings and contribute to deflationary pressure, while squeezing restaurant profits, hiring, and income growth, which then undermines domestic consumption.

Summary

China Update News this week shows a cautious mix of signals: industrial profits are improving, but energy costs may quickly pressure margins; infrastructure projects like Chongqing’s Goddess Escalator demonstrate continued reliance on policy-controlled demand; public science funding is accelerating toward potential global leadership; and Beijing is moving to end the delivery subsidy war in favor of competition based on efficiency and service.