Happy Saturday, and welcome to another round of China Update News, where the focus is on what is changing in China’s economy and what those shifts mean beyond its borders. This week’s story starts with an unusual level of frankness from China’s top Communist Party theoretical publication, then moves through softer signals in services demand, intensifying China-to-Australia vehicle competition, and finally the growing friction between China’s diplomatic posture and the energy realities of the Iran war.

Table of Contents

- 1) China Update News: Party Journal Admits Export-Led Growth Is Unsustainable

- 2) Can China Reduce Its Trade Surplus Without More Debt?

- 3) China Update News: Services Sector Grows, but Momentum Fades

- 4) China Update News: China Becomes Australia’s Top Source of Imported Vehicles

- 5) China Update News: China’s Iran War Position Faces a Core Contradiction

- 6) The energy reality: China tries to cushion shocks while costs rise

- 7) Drone supply networks add another layer of complication

- What China’s “responsible actor” test really is

- FAQ

1) China Update News: Party Journal Admits Export-Led Growth Is Unsustainable

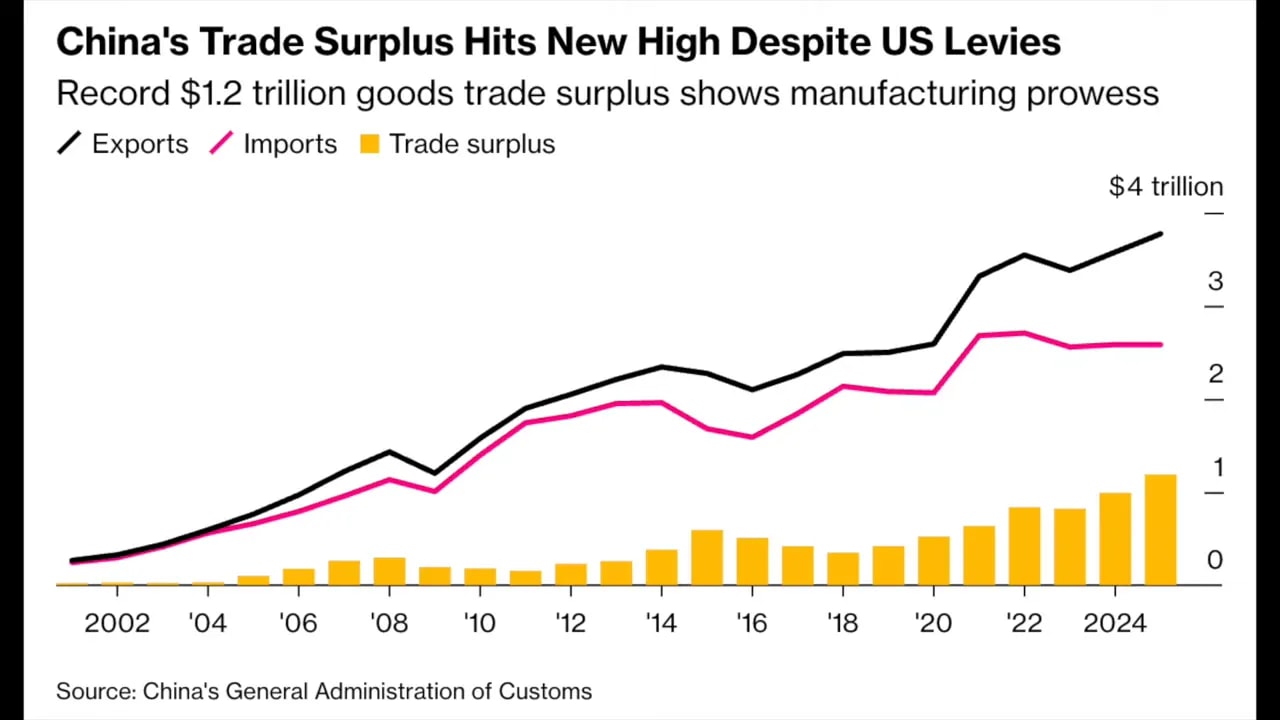

China’s top Communist Party journal has now acknowledged something that many analysts have been warning about for years: the country needs to move away from an export-driven growth model because it has become unsustainable.

The admission appears in a commentary published in Qiushi, the party’s flagship theoretical journal. The key theme is that both internal and external conditions shaping China’s trade balance have entered a phase of “profound changes.”

What China says is going wrong

The commentary points to structural weaknesses that have limited the quality of China’s export performance. In particular:

- Low domestic value added in exports

- Limited competitiveness in high-end manufacturing and critical technologies

In other words, it is not only that exports are changing. It is that the model China used to scale up growth is facing constraints that go deeper than near-term demand swings.

The policy direction: less surplus, more balanced trade

The implied direction is a strategic recalibration. Rather than treating export surpluses as the engine of growth, policymakers are increasingly emphasizing:

- Strengthening domestic demand

- Upgrading industrial capacity

- Improving the quality of trade

The commentary also frames the export-led model that powered decades of rapid expansion as no longer viable at China’s current scale. That is a major signal because it shifts the narrative from “exports are the solution” toward “exports are a problem that must be managed.”

Why this matters right now

Beijing’s acknowledgement arrives at a sensitive moment. China’s record trade surplus last year unsettled major trading partners and renewed concerns about a potential “China shock 2.0.” At the same time, geopolitical tensions have increased fears of supply chain disruptions.

So the question becomes: is China admitting unsustainability because it wants to reduce tensions, or because the economic model genuinely cannot keep working the way it did?

Beijing’s current framing, according to the commentary’s logic, is that China’s surplus is not necessarily a deliberate pursuit, but rather a byproduct of strong manufacturing capacity and resilient supply chains. That may be the official story. But the emphasis on rebalancing is clearly meant to reshape external expectations.

What “quality trade” looks like in practice

On the export side, the approach emphasizes growth in areas like:

- High-end equipment

- Green and low-carbon products

- Advanced intermediate goods

- Expansion in services and digital trade

It also calls for deeper integration between domestic and international trade systems, including aligning standards more closely with global trade rules.

This is important because it suggests the effort is not only about selling less. It is about selling differently, in markets and categories where China wants to be more competitive without relying on the same export economics of the past.

2) Can China Reduce Its Trade Surplus Without More Debt?

A finance professor at Peking University, Michael Pettis, reacted quickly to the admission. The central idea: Beijing is officially recognizing that its trade policies are unsustainable, and a more balanced trade is inevitable. But the follow-up question is how China will get there.

The most interesting part of the analysis is the professor’s framing of three main ways China can reduce a trade surplus. Each option comes with significant costs and trade-offs.

Three routes to a lower surplus

Cut production and accept slower GDP growth.

This reduces exports, but at the price of weaker overall economic momentum.

Increase investment growth sharply.

However, the analysis notes that it is not easy to find investment opportunities that do not worsen excess capacity. That means boosting investment can lead to faster growth in the debt burden.

Boost the growth rate of consumption.

But unless consumption growth is funded by even faster growth in debt, it implies a structural shift where China’s share of global manufacturing would decline.

So the core tension is this: balancing trade is not only a trade policy issue. It is also a macroeconomic and debt constraint issue.

What happens next depends on the rest of the world

The analysis concludes that the pace of China’s push toward balanced trade will likely match how quickly other countries protect their domestic manufacturing industries. That, in turn, is influenced by how quickly the United States reduces its trade deficit.

This is a reminder that trade balances are not only made inside China. They are also shaped by global demand patterns, industrial policy, and tariff and non-tariff barriers abroad.

3) China Update News: Services Sector Grows, but Momentum Fades

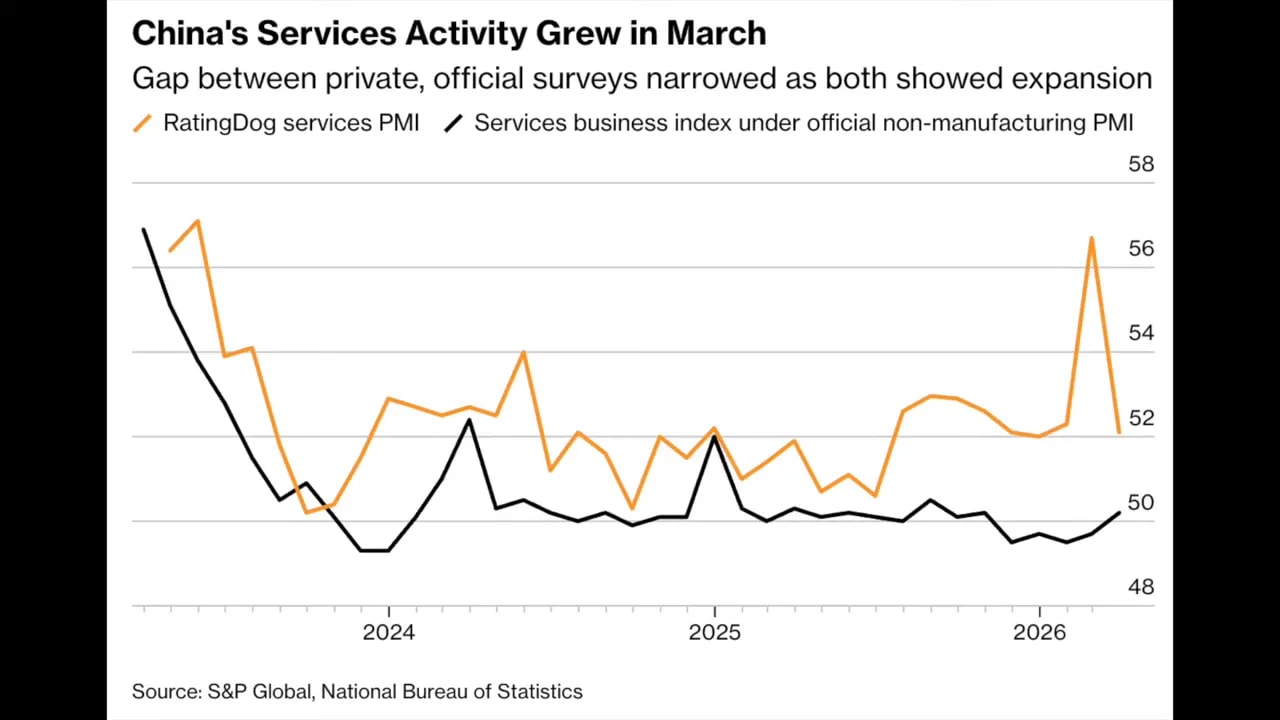

Beyond trade, the next signal in this China Update News round comes from services. Officially, services activity improved in March. But the improvement was not strong enough to eliminate concerns that consumer demand remains fragile.

Private survey: services slowed sharply

According to a private survey, the Rating Dog China Services Purchasing Managers Index fell to 52.1 in March from 56.7 in February. Expectations were missed, and the slowdown was sharp.

The headline PMI remains above the 50 threshold that separates expansion from contraction. But the drop signals that momentum is fading after a temporary surge linked to February’s extended lunar new year holiday.

Divergence between headline numbers and underlying demand

The data highlights a separation between what the index suggests and what households are actually doing. Even where services activity improved overall, gains were largely concentrated in producer services such as finance.

Consumer-facing services, including retail and catering, continued to contract. That is a direct indicator of how cautious households remain with spending.

Deflationary pressure shows up in pricing

The March services picture also includes building cost pressures. Services firms reported higher input costs due to rising fuel, materials, and labor expenses. Yet businesses were not fully able to pass those higher costs onto consumers.

Instead, firms cut selling prices for the third time in four months in an effort to stimulate demand. That behavior is consistent with deflationary pressure, where prices fall or fail to rise despite higher underlying costs.

Why the policy challenge is hard

Beijing has emphasized rebalancing the economy toward domestic demand again and again, with services as a key pillar of the transition. However, the task is complicated by:

- Lowered growth targets to 4.5%

- Scaled-back fiscal support

As a result, shifting away from investment and exports is likely to be a slower and more difficult process than Beijing had hoped.

4) China Update News: China Becomes Australia’s Top Source of Imported Vehicles

Another major development in China Update News is not about China’s balance of trade directly, but about how Chinese manufacturing is competing in a developed, high-income auto market.

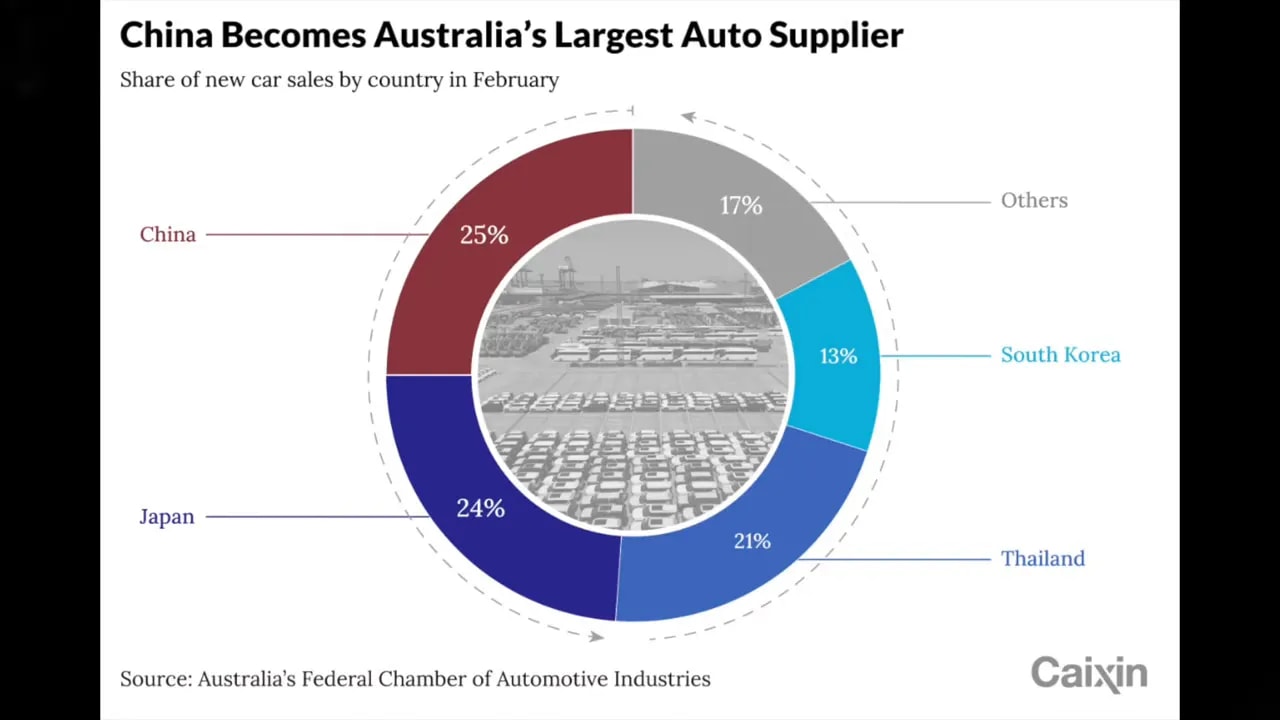

China has overtaken Japan as Australia’s largest source of imported vehicles for the first time. Australia imported 22,300 vehicles from China in February, giving China a 25% market share. Japan, which had dominated since 1998, is now in second place.

Why Australia is a useful “barometer”

The reasoning for tracking Australia is straightforward: Australia has relatively few tariffs and other barriers on car imports compared with some other Western economies. In places like the US or Europe, high barriers can reduce the ability of foreign brands, including Chinese brands, to compete on price and variety.

So Australia offers a clearer window into how globally made vehicles compete when market access is relatively open.

Chinese brands and global brands driving change

This shift reflects the rise of Chinese automakers and China’s role as a manufacturing hub for international brands. Companies such as BYD, Geely, and Xpeng expanded in Australia, and Chinese-made vehicles produced for global firms, including Tesla and BMW, are also part of the story.

Chinese brands now account for around 20% of Australia’s new car market, up from less than 5% in 2020.

Price competitiveness, SUVs, and electrification

Much of the growth is attributed to competitively priced SUVs, pickups, and electrified vehicles.

In the first two months of 2026, four Chinese automakers ranked among Australia’s top 10 best-selling brands, led by BYD, whose sales surged year over year.

A global trend beyond Australia

The broader implication is that China is no longer only the world’s largest car market. It is increasingly a dominant exporter of vehicles and automotive technology.

That matters for other economies because it implies Chinese supply chains and manufacturing capabilities are scaling to compete internationally, not just domestically.

5) China Update News: China’s Iran War Position Faces a Core Contradiction

The final segment of this China Update News package moves from economics into geopolitics, where the stakes include shipping, energy costs, and the limits of diplomacy.

As the Iran war intensifies, Beijing is trying to position itself as a diplomatic stabilizer and an economic shock absorber. But those roles are increasingly in tension.

Diplomatic outreach and what is missing

Over the past 48 hours, China’s foreign minister Wang Yi reportedly held talks with counterparts from Germany, Saudi Arabia, Bahrain, and the European Union, and also had earlier conversations with Iran.

What stands out is the absence of confirmed calls with US or Israeli officials in the most sensitive channels of the conflict. That suggests limits in China’s reach where military and security decisions are most tightly held.

Beijing’s public line: blame shifts, ceasefire focus

Publicly, China has argued that disruptions in the Strait of Hormuz are driven by US and Israeli military actions and that a ceasefire, not military intervention, is the path to restoring safe passage.

China’s stance does not directly blame Tehran for targeting the passage or for using the disruption as leverage in peace talks.

However, that narrative is shaping Beijing’s behavior at the United Nations. China opposed a resolution backed by Britain that would have authorized “all necessary means” to protect shipping. Chinese officials argued that such language risks legitimizing escalation.

Critics argue this creates a gap between rhetoric and action

Critics say the approach underscores Beijing’s reluctance to take concrete steps to reopen one of the world’s most critical energy chokepoints.

Beijing may also be concerned about alienating its relationship with Tehran, especially if it appears to align with actions that Tehran opposes. But the tension is growing as global pressure mounts and the gap between what is said and what is done becomes more visible.

6) The energy reality: China tries to cushion shocks while costs rise

While diplomacy is constrained, China is moving aggressively on the economic front, particularly where energy security is at stake.

Maintain fuel production even at a loss

Authorities ordered domestic refiners to keep fuel production at or above last year’s level, even if it results in losses. The rationale is clear: prevent supply disruptions amid instability around the Strait of Hormuz.

Quiet energy arbitrage boosts Asia’s middlemen role

China is also leveraging its position in global energy markets. Chinese firms reportedly resold record volumes of liquefied natural gas to countries such as South Korea, Japan, and India, benefiting from tight supply conditions.

This arbitrage has turned China into a key middleman in Asia’s energy flows, even while the country grapples with higher domestic costs.

Costs are rippling into airlines and broader markets

The impact is showing up in the corporate market. Chinese airlines, including Air China, China Eastern Airlines, and China Southern Airlines, have seen sharp declines in share prices as fuel expenses surge.

The sector that might have benefitted from rerouted global traffic instead appears to be an early casualty of the energy shock.

Across Asia: fuel shortages, inflation, and fiscal strain

Beyond China, the conflict’s impact is spreading across Asia. Governments are dealing with fuel shortages, inflation pressures, and fiscal strain. The region’s priorities are shifting from long-term great power competition toward immediate economic survival.

7) Drone supply networks add another layer of complication

There are also growing concerns about Iran’s ability to sustain its military capabilities. Reports suggest Tehran is using complex global supply networks across multiple countries to source components for drones, with some supplies allegedly linked to Chinese and Russian suppliers.

While such claims are difficult to fully verify, they risk complicating China’s diplomatic positioning. If even parts of those allegations are credible, they would challenge the credibility of any position China takes as a neutral stabilizer.

What China’s “responsible actor” test really is

Taken together, the crisis exposes a contradiction at the heart of China’s approach. Beijing wants to be seen as a responsible global actor advocating stability while avoiding entanglement in military solutions. But as the conflict drags on, neutrality becomes harder to maintain.

The Strait of Hormuz remains the central test. If China helps broker de-escalation or facilitates safe passage, its global standing could strengthen. If it cannot, it risks being seen as a bystander offering limited solutions, despite years of positioning itself as a major power capable of shaping an alternative global order.

FAQ

What did China’s party journal say about the export model?

It acknowledged that China must move away from an export-driven growth model, calling it unsustainable. The commentary cited structural weaknesses such as low domestic value added in exports and limited competitiveness in high-end manufacturing and critical technologies.

Why is China’s trade surplus rebalancing difficult?

Because the main pathways to reduce a surplus come with trade-offs: cutting production means slower GDP growth; boosting investment can increase debt and worsen excess capacity; boosting consumption requires either major structural change or financing that can raise debt further.

What do the services indicators suggest for demand?

They suggest momentum is fading after a holiday-linked boost. Growth is not evenly distributed, with producer services (like finance) holding up more than consumer-facing sectors (like retail and catering), and pricing behavior pointing to continued deflationary pressure.

How significant is China’s vehicle export shift into Australia?

Australia imported 22,300 vehicles from China in February, giving China a 25% market share and making it the top source of imports for the first time, surpassing Japan.

How is the Iran war affecting China’s economy?

China is prioritizing energy security by ordering refiners to maintain fuel production, using energy market activity such as LNG resales, and managing rising costs that are already visible in sectors like aviation.